1 November 2017

Q2FY18 Results Update | Sector: Telecom

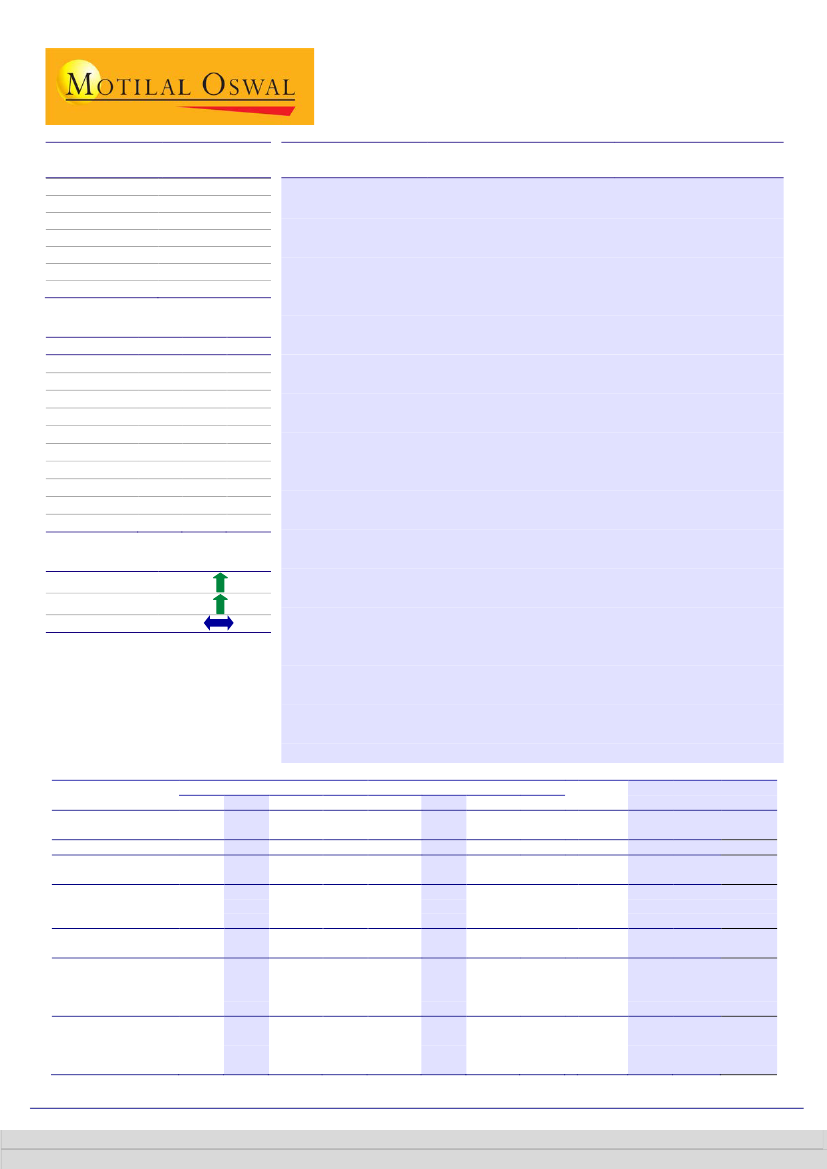

Bharti Airtel

Buy

BSE SENSEX

33,600

Bloomberg

Equity Shares (m)

M.Cap.(INRb)/(USDb)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

Avg Val, INRm

Free float (%)

our est., but flat EBITDA margin of 34.4% implies a beat of 180bp to our est.

Lean cost structure supports strong EBITDA growth:

Bharti has created a

Financials & Valuations (INR b)

2017 2018E 2019E

lean cost structure. This is evident from Africa’s 800bp margin improvement

Y/E Mar

954.7 875.8 946.3

Net Sales

in the last four quarters, despite a 2% revenue decline YoY. India wireless too

353.3 314.5 348.1

EBITDA

has seen a 7%/1% YoY decline in network/employee cost, despite accelerated

45.3

15.0

25.8

PAT

network rollout. We believe this offers Bharti strong ARPU sensitivity to

11.3

3.8

6.5

EPS (INR)

EBITDA, which should drive healthy operating leverage, as ARPU recovers in

-4.6 -66.9

72.2

Gr. (%)

FY19E.

168.8 171.0 176.3

BV/Sh (INR)

Expect India ARPU recovery in FY19 to drive growth:

RJio has taken four

6.8

2.2

3.7

RoE (%)

price actions since turning paid, signaling ARPU accretion, which has been

5.4

3.8

4.9

RoCE (%)

hostage to competition. Post IUC and Jiophone launch impact in 2HFY18, we

47.5 143.4

83.3

P/E (x)

believe ARPUs should improve from FY19. Bharti’s strong spectrum/data

3.2

3.1

3.1

P/BV (x)

network portfolio and data volume of meager 260m GB (i.e. less than one

fifth of RJio) indicate a huge scope to improve ARPUs (26% below pre-RJio

launch) through value-accretive offerings. Management’s guidance of 25%

Estimate change

capex increase to INR250b should therefore be more front-loading and

TP change

reduce capex beyond 3-4 quarters.

Rating change

Maintain Buy with revised TP of INR680:

We have revised consol. EBITDA by

2/5% for FY18/19E due to higher Africa EBITDA. We expect consol. EBITDA

growth of -11%/11% in FY18/19E on an 8% India wireless EBITDA recovery in

FY19E. We have revised our SOTP-based TP to INR680 v/s INR490 earlier, led

by a) reducing Africa biz’s equity value to -INR25 v/s -INR80 earlier; and b)

improving India biz’s equity value to INR583, assigning 10.5x EV/EBITDA on

Sept’19 EBITDA. Bharti can offer 7-8% FCF yield as the market bottoms out.

Quarterly Performance (Consolidated)

Y/E March

Gross Revenue

YoY Change (%)

Total Expenditure

EBITDA

Margins (%)

Depreciation

Interest

Other Income

PBT before EO expense

Extra-Ord expense

PBT

Tax

Rate (%)

MI & P/L of Asso. Cos.

Reported PAT

Adj PAT

YoY Change (%)

Margins (%)

1Q

2Q

2,55,465 2,46,515

7.9

3.4

1,59,985 1,52,113

95,480 94,402

37.4

38.3

50,402 49,560

19,399 19,057

2,787

1,568

28,466 27,353

3,536

66

24,930 27,287

10,089 11,136

40.5

40.8

222

1,544

14,619 14,607

16,724 14,646

70.7

25.9

6.5

5.9

FY17

FY18

FY17

9,54,683

-1.1

6,01,386

3,53,297

37.0

1,97,730

76,974

10,336

88,929

11,697

77,232

34,819

45.1

4,416

37,997

45,291

-4.6

4.7

FY18E

8,75,838

-8.3

5,61,372

3,14,466

35.9

2,01,231

81,267

15,419

47,386

2,289

45,097

21,701

48.1

9,539

13,857

15,008

-66.9

1.7

2QFY18E

2,16,555

-12.2

1,41,536

75,018

34.6

49,282

21,459

3,698

7,975

0

7,975

4,380

54.9

1,458

2,138

2,138

-85.4

1.0

Var (%)

0.6

-2.1

5.6

173.6

3Q

4Q

1Q

2Q

3QE

4QE

2,33,357 2,19,346 2,19,581 2,17,769 2,16,952 2,21,535

-3.0

-12.1

-14.0

-11.7

-7.0

1.0

1,48,542 1,40,746 1,41,997 1,38,549 1,39,102 1,41,724

84,815 78,600 77,584 79,220 77,851 79,811

36.3

35.8

35.3

36.4

35.9

36.0

48,350 49,418 48,192 46,873 53,083 53,083

19,356 19,162 18,274 23,266 19,985 19,742

3,487

2,494

3,698

3,907

3,907

3,907

20,596 12,514 14,816 12,988

8,689

10,893

2,040

6,055

503

1,786

0

0

18,556

6,459

14,313 11,202

8,689

10,893

11,841

1,753

8,136

5,341

3,650

4,575

63.8

27.1

56.8

47.7

42.0

42.0

1,678

972

2,504

2,431

2,043

2,561

5,037

3,734

3,673

3,430

2,997

3,757

5,775

8,146

3,890

4,364

2,997

3,757

-54.6

-45.5

-76.7

-70.2

-48.1

-53.9

2.5

3.7

1.8

2.0

1.4

1.7

S&P CNX

10,441

BHARTI IN

Cost-structuring measures show results

3,997

Africa delivers, finally:

Consol. EBITDA of INR79.2b was up only 2% QoQ (-

2,152.2 / 33.3

16% YoY, 6% beat) due to a 1% QoQ drop in revenue. Africa surprised with a

545 / 284

7% QoQ revenue jump (-2% YoY) to INR52b, backed by a 5% dollar ARPU rise;

31/44/49

Africa EBITDA surged 23% QoQ to INR16.8b on a leaner cost structure. India

1,733.5

wireless revenue drop of 5% QoQ (-17% YoY) to INR122.5b was in line with

32.9

CMP: INR538

TP: INR680 (+26%)

62.9

40.5

60.4

Aliasgar Shakir – Research analyst

(Aliasgar.Shakir@motilaloswal.com); +91 022 6129 1565

Hafeez Patel – Research analyst

(Hafeez.Patel@motilaloswal.com); +91 22 3010 2611

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.