Sector Update| 1 November 2017

Automobiles

Maruti Suzuki

CMP: INR8,235

Stock Info

Bloomberg

Equity Shares (m)

M.Cap. (INR b)/(USD b)

52-Week Range (INR)

1, 6, 12 Rel. Per (%)

TP: INR9,466 (+15%)

Buy

MSIL IN

302.1

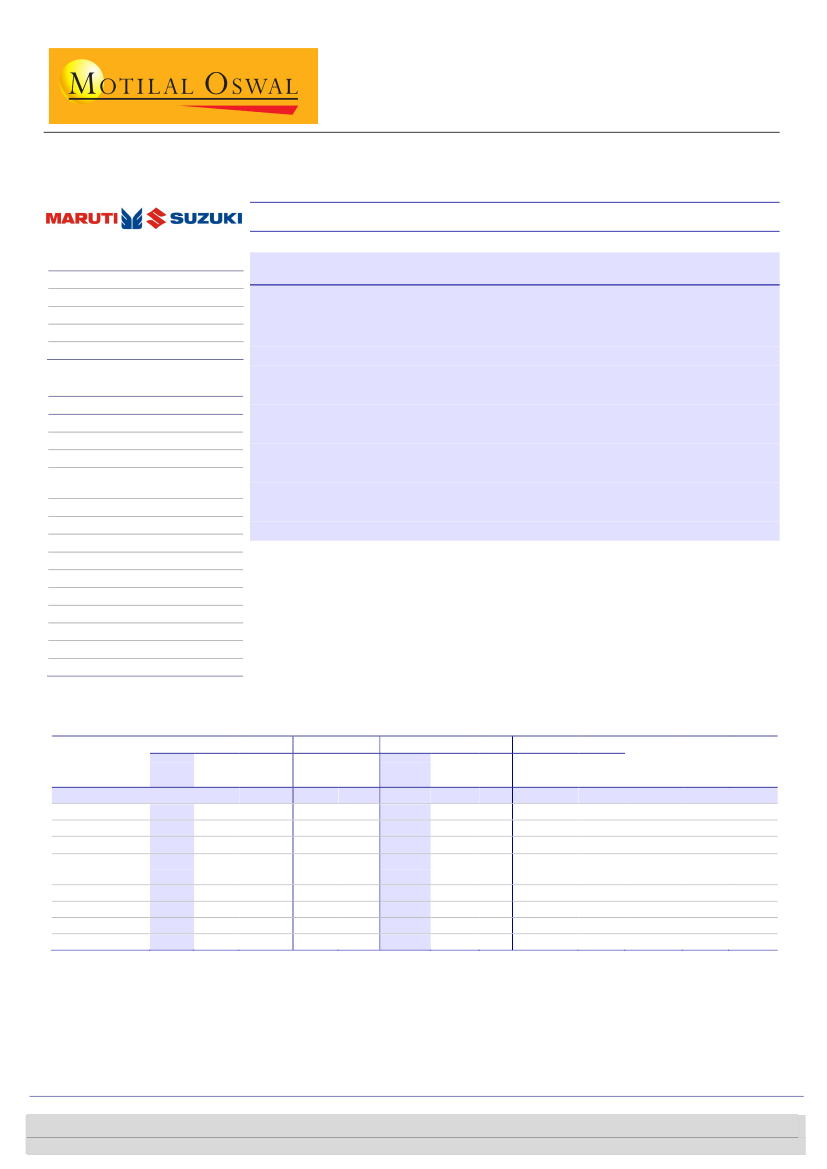

Domestic sales grew 9.9% YoY to 136k

2488/38.5

8283/4770

MSIL’s Sep-17 wholesales came in at 146,446 units (+9.5% YoY), marginally lower than

-4/13/20

our estimate of 150,456 units. YTD growth was at 14.7%, with a residual monthly run-

Volumes up 9.5% YoY to 146.4k units (below est. of 150.5k)

Financials Snapshot (INR b)

Y/E MARCH 2018E 2019E 2020E

Sales

800.4 956.2 1,103.0

EBITDA

124.8 159.1 183.8

Adj. PAT

85.3 113.3 133.3

Adj. EPS

(INR)*

288.1 381.0 447.8

EPS Gr. (%)

15.8 32.3

17.5

BV/Sh. (INR) 1,378 1,632 1,930

RoE (%)

20.5 23.0

22.9

RoCE (%)

28.6 31.7

31.4

Payout (%)

36.2 32.1

32.7

Valuations

P/E (x)

28.6 21.6

18.4

P/CE (x)

21.7 17.0

14.6

EV/EBITDA (x) 17.3 13.1

10.9

Div. Yield (%)

1.0

1.2

1.5

*Cons.

Snapshot of volumes for Oct-17

YoY

Company Sales

Maruti Suzuki

LCVs

Vans

Mini Segment

Compact (incl

Dzire Tour)

Mid Size - CIAZ

UVs

Total Domestic

Export

Oct-17 Oct-16

146,446 133,793

872

80

12,669 12,790

32,490 33,929

62,480 52,597

4,107 6,360

23,382 18,008

136,000 123,764

10,446 10,029

rate of 153k units.

Domestic volumes grew 9.9% YoY to 136k (est. of 139.5k), led by growth in the

compact (+18.8% YoY) and UV (+29.8% YoY) segments.

Growth in the compact segment was led by Baleno and new Dzire, while that in UVs

was led by Brezza and new S-cross.

Ciaz sales declined 35.4% YoY to 4.1k (est. of 4.8k).

Export volumes increased 4.2% YoY to 10,446 units (est. of 11,000 units).

The stock trades at 28.6x/21.6x FY18E/19E consol. EPS of ~INR281/375. Maintain Buy.

MoM

YoY (%)

MoM

Sep-17

FY18YTD FY17YTD

chg

(%) chg

9.5

163,071 -10.2 1,033,135 900,706

879

-0.8

4,229

163

-0.9

13,735 -7.8

91,788 90,545

-4.2

38,479 -15.6 252,217 241,588

18.8

-35.4

29.8

9.9

4.2

72,804

5,603

19,900

151,400

11,671

-14.2

-26.7

17.5

-10.2

-10.5

427,726

38,242

147,630

961,832

71,303

348,901

37,970

109,967

829,134

71,572

(%)

chg

14.7

1.4

4.4

22.6

0.7

34.2

16.0

-0.4

FY18

estimate

1,798,133

8,000

161,802

432,948

760,103

63,159

245,218

1,671,231

126,902

Residual

Growth

Gr. (%)

(%)

14.6

14.5

6.4

4.6

30.0

-2.0

25.3

15.7

2.3

13.9

4.8

40.9

-5.9

13.8

15.3

5.9

Residual FY18 YTD

Monthly Monthly

Run rate Run rate

153,000 147,591

754

604

14,003 13,113

36,146 36,031

66,475

4,983

19,518

141,880

11,120

61,104

5,463

21,090

137,405

10,186

Jinesh Gandhi - Research analyst

(Jinesh@MotilalOswal.com); +91 22 3982 5416

Research analyst: Deep Shah

(Deep.S@MotilalOswal.com); +91 22 6129 1533 /

Suneeta Kamath

(Suneeta.Kamath@MotilalOswal.com); +91 22 6129

1534

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.