Sector Update | 21 November 2017

Sector Update | Financials

Financials - NBFC

Technology

MSME financing for NBFCs faster

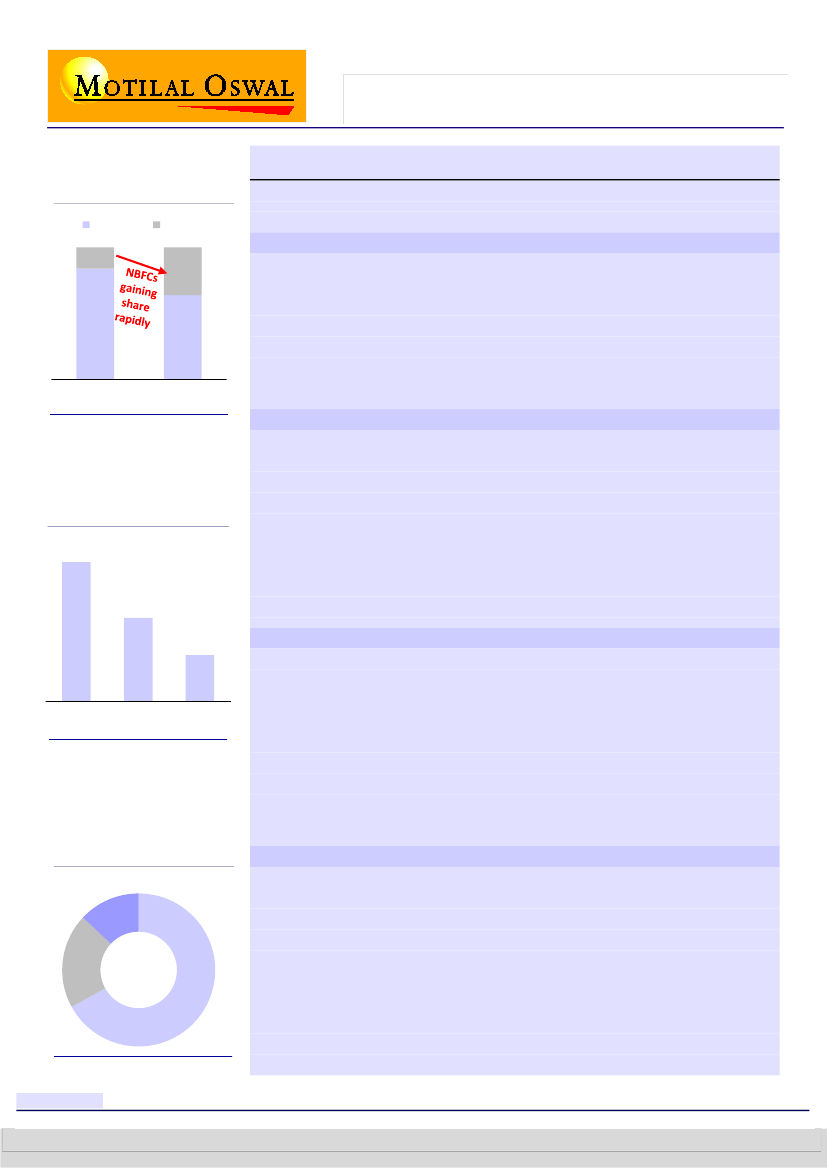

than banks resulting in higher

share for NBFCs (%)

Banks (%)

8

NBFC (%)

MSME lending – Challenging outlook

LAP losing its sheen; some dilution in underwriting standards

CRISIL conducted a webinar on its outlook for the MSME financing sector in India.

NBFCs gaining market share rapidly

18

92

82

FY12

FY17

Against overall system-wide credit growth of ~9% in the past 5 years, the MSME

lending book of banks and NBFCs grew at 13% CAGR to INR14tn currently. With a

more customer-centric, on-the-ground approach, NBFCs have achieved stronger

growth than banks with their MSME lending book growing at 32% CAGR vis-a-vis

10% for banks. Consequently, their market share increased from 8% in FY12 to 18%

in FY17.

Going forward, NBFCs are expected to grow this book at ~20% CAGR,

while that of banks should grow at ~9% CAGR.

LAP a key driver of MSME lending…

As is well known, LAP has been a focused product for several NBFCs over the past

few years, given large scalability potential, attractive margins and modest

delinquencies.

As a result, the LAP portfolio (for banks and NBFCs) grew at 26%

CAGR over FY12-17 as compared to 10% CAGR over the same time period for non-

LAP MSME financing.

It now accounts for 24% of overall MSME lending, compared

to 15% in FY12. For NBFCs alone, it accounts for 67% of the MSME lending book.

However, given increased competition, declining margins and lower demand post

demonetization and GST, the

LAP portfolio is expected to growth at 13-15% CAGR

over the next two years, reaching a size of ~INR4.2t by FY19.

Margins in LAP on the decline (%)

4-4.5

3.7-4.2

3.5-4

…but losing its sheen, of late

In the first half of the decade, NBFCs engaged in LAP enjoyed strong growth with

superior margins, and thus, very good return ratios. However, with increasing

competition over the years, attractiveness of the sector has somewhat faded.

As per

CRISIL, NIMs for NBFCs in LAP declined 30bp from 4-4.5% in FY16 to 3.7-4.2% in

FY17 and is expected to reduce another 20bp in FY18.

At the same time, given

increased delinquencies, GNPL ratio (2-year lagged) increased from 3.1% to 3.9%

over FY15-17. For the whole MSME portfolio of NBFCs, the GNPL ratio increased

from 2.9% to 6.1% over the same time period. Asset quality is expected to worsen in

the near term due to GST-related challenges faced by the unorganised sector.

FY16

FY17

FY18E

Mix for NBFCs – LAP is bulk of

MSME credit

MSME

Secured,

13%

Un-

secured ,

20%

Intense competition leading to moderation in underwriting standards

A key trend observed by CRISIL is that NBFCs have been migrating more towards

lower-ticket LAP due to better yields and lesser competition. Apart from this, there

have been some concerning trends of dilution in underwriting standards witnessed

over the past few quarters. For example, in order to maintain yields,

the share of

commercial properties taken as mortgage for LAP has increased.

Similarly, the

share of unsecured lending by NBFCs is on the rise.

While it currently stands at

20% of overall MSME lending, on an incremental basis, 35% of disbursements are

unsecured. In addition, there have been cases of 3-4 year loan tenures of unsecured

loans being given today (v/s average of 1-2 years). Also, as per CRISIL,

around 35-

40% of disbursements in LAP are balance transfer cases.

LAP, 67%

Research Analyst: Alpesh Mehta

(Alpesh.Mehta@MotilalOswal.com); +91 22 3982 5415

|

Piran Engineer

(Piran.Engineer@MotilalOswal.com); +91 22 3980 4393

Nitin Aggarwal

(Nitin.Aggarwal@MotilalOswal.com); +91 22 3982 5540

| Anirvan Sarkar

(Anirvan.Sarkar@MotilalOswal.com); +91 22 3982 5505

21 November 2017

1

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.