24 November 2017

Market snapshot

Equities - India

Close

Chg .%

Sensex

33,588

0.1

Nifty-50

10,349

0.1

Nifty-M 100

19,884

0.3

Equities-Global

Close

Chg .%

S&P 500

2,597

0.0

Nasdaq

6,867

0.0

FTSE 100

7,417

0.0

DAX

13,009

0.0

Hang Seng

11,737

-1.9

Nikkei 225

22,523

0.0

Commodities

Close

Chg .%

Brent (US$/Bbl)

63

0.2

Gold ($/OZ)

1,291

-0.1

Cu (US$/MT)

6,937

0.2

Almn (US$/MT)

2,097

0.4

Currency

Close

Chg .%

USD/INR

64.6

-0.5

USD/EUR

1.2

0.2

USD/JPY

111.2

0.0

YIELD (%)

Close

1MChg

10 Yrs G-Sec

7.0

0.0

10 Yrs AAA Corp

7.8

0.0

Flows (USD b)

23-Nov

MTD

FIIs

0.0

2.3

DIIs

0.0

1.1

Volumes (INRb)

23-Nov

MTD*

Cash

341

394

F&O

11,340

6,813

Note: YTD is calendar year, *Avg

YTD.%

26.1

26.4

38.6

YTD.%

16.0

27.6

3.8

13.3

24.9

17.8

YTD.%

14.2

12.1

25.6

23.1

YTD.%

-4.9

12.7

-4.9

YTDchg

0.5

0.2

YTD

7.8

12.5

YTD*

306

5,630

Today’s top research idea

Bajaj Auto: Back on recovery path

Volume growth coupled with improving mix to drive margin expansion

Domestic 3W:

Strong medium-term visibility as regulatory changes in key

states (where BJAUT enjoys over 90% share) are opening-up incremental

opportunity of ~142k passenger 3W (v/s 240k sales in FY17).

Exports:

Stability in key markets, ramp-up in new markets drive recovery,

exports grew by 9.4% YTDFY18, avg. volumes of 135.3k/month (v/s avg

117.6k/month in FY17).

Domestic motorcycle:

Recovery driven by plugging portfolio gaps, recent

launch of ES variants in Economy and Pulsar 160NS in Premium.

KTM/Husqvarna contract manufacturing volumes could multiply by 3x in a few

years, Triumph would enable entry in mid-capacity cruiser segment (250-

750cc).

Improvement in market/ product mix could lead to EBITDA margin expansion of

~340bp to 22% by FY19 (v/s est. of 20.6%).

Broad-based recovery to drive ~16% EPS CAGR over FY17-20.

Buy

with TP of

~INR4,197.

Research covered

Cos/Sector

Bajaj Auto

Bata India

Monsanto India

Key Highlights

Back on recovery path

Premiumization to support margin expansion

Results below estimates

Piping hot news

President clears stricter version of Insolvency and Bankruptcy Code

President Ram Nath Kovind gave his assent to an ordinance amending the

Insolvency and Bankruptcy Code (IBC) on Thursday, barring errant promoters

of defaulting companies from regaining control of their assets being sold

under the bankruptcy process…

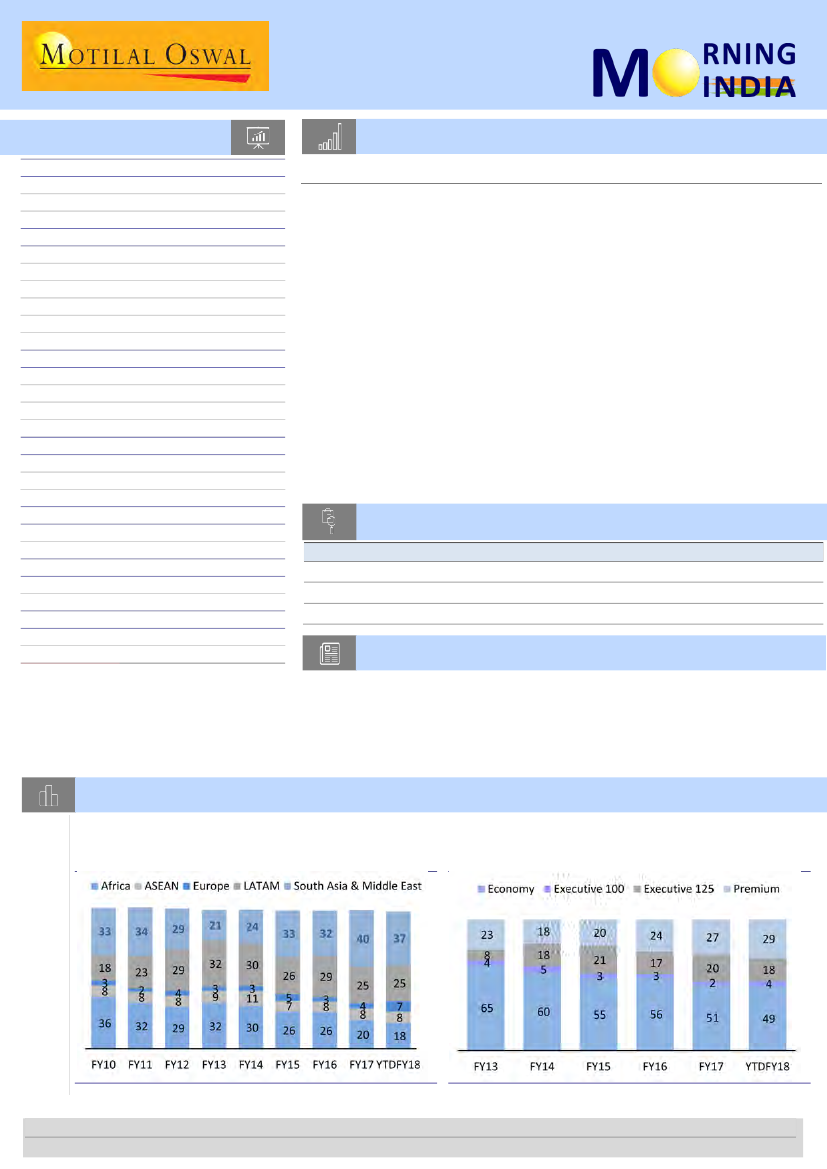

Chart of the Day: Bajaj Auto – Back on recovery path

Africa’s contribution to motorcycle exports from India

reduces significantly over the years, as LATAM and

SA/ME share increases

Export mix shifts in favor of premium products

Research Team (Gautam.Duggad@MotilalOswal.com)

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.