4 December 2017

Market snapshot

Equities - India

Close

Chg .%

Sensex

32,833

-1.0

Nifty-50

10,122

-1.0

Nifty-M 100

19,692

-1.0

Equities-Global

Close

Chg .%

S&P 500

2,642

-0.2

Nasdaq

6,848

-0.4

FTSE 100

7,300

-0.4

DAX

12,861

-1.2

Hang Seng

11,449

-0.2

Nikkei 225

22,819

0.4

Commodities

Close

Chg .%

Brent (US$/Bbl)

64

1.4

Gold ($/OZ)

1,281

0.4

Cu (US$/MT)

6,809

1.1

Almn (US$/MT)

2,059

1.2

Currency

Close

Chg .%

USD/INR

64.5

0.2

USD/EUR

1.2

0.0

USD/JPY

112.2

-0.3

YIELD (%)

Close

1MChg

10 Yrs G-Sec

7.1

0.03

10 Yrs AAA Corp

7.8

0.02

Flows (USD b)

1-Dec

MTD

FIIs

0.0

3.1

DIIs

0.0

1.5

Volumes (INRb)

1-Dec

MTD*

Cash

329

387

F&O

4,413

6,910

Note: YTD is calendar year, *Avg

YTD.%

23.3

23.7

37.2

YTD.%

18.0

27.2

2.2

12.0

21.9

19.4

YTD.%

14.9

11.1

23.3

20.8

YTD.%

-5.1

13.1

-4.1

YTDchg

0.5

0.3

YTD

8.6

12.8

YTD*

307

5,670

Today’s top research idea

NMDC: Iron ore pricing improving

Highly profitable steel project, albeit delayed, is available for free

NMDC has increased iron ore prices by 10-13% as Indian iron ore mines are

regaining price power. We expect NMDC’s iron ore volumes to grow at 5-6% over

the next 4-5 years from its existing mines that are currently operating at ~80%

utilization.

Investment in rail evacuation line and growth at its key customers will drive

volume growth. Steel plant, though delayed, will be highly profitable given

technology efficiency, scale advantage and raw material sourcing. Margins in the

steel business are likely to be 10,000/t.

Despite factoring in 10% lower iron ore margins w.r.t. FY18, we expect EBITDA

CAGR of 17% to INR97b over FY17-22. We expect equity value CAGR of 15% to

INR223 in four years, while the dividend yield will be ~5% at CMP. Thus, we

expect a 20% annual total stock return over the next 3-4 years.

Research covered

Cos/Sector

NMDC

Infosys

Biocon

Persistent Systems

Utilities

Automobiles

Key Highlights

Iron ore pricing improving

New era Take#2; Appoints CapGemini’s Salil Parekh as CEO and MD

Mylan/ Biocon received Trastuzuman approval in US

Solutions in sight; Analyst Day Takeaways

CESC wins 100MW in BEST’s PPA, Tata Power at loss

Volumes numbers (November 2017)

Piping hot news

Reviving growth tops Infosys boss Salil Parekh’s agenda

Infosys will seek to revive growth and create a fresh team of leaders when

chief executive Salil Parekh takes charge in January at the Bengaluru company,

which has battled nearly a year of internal turmoil and slashed revenue

forecast for the fiscal year…

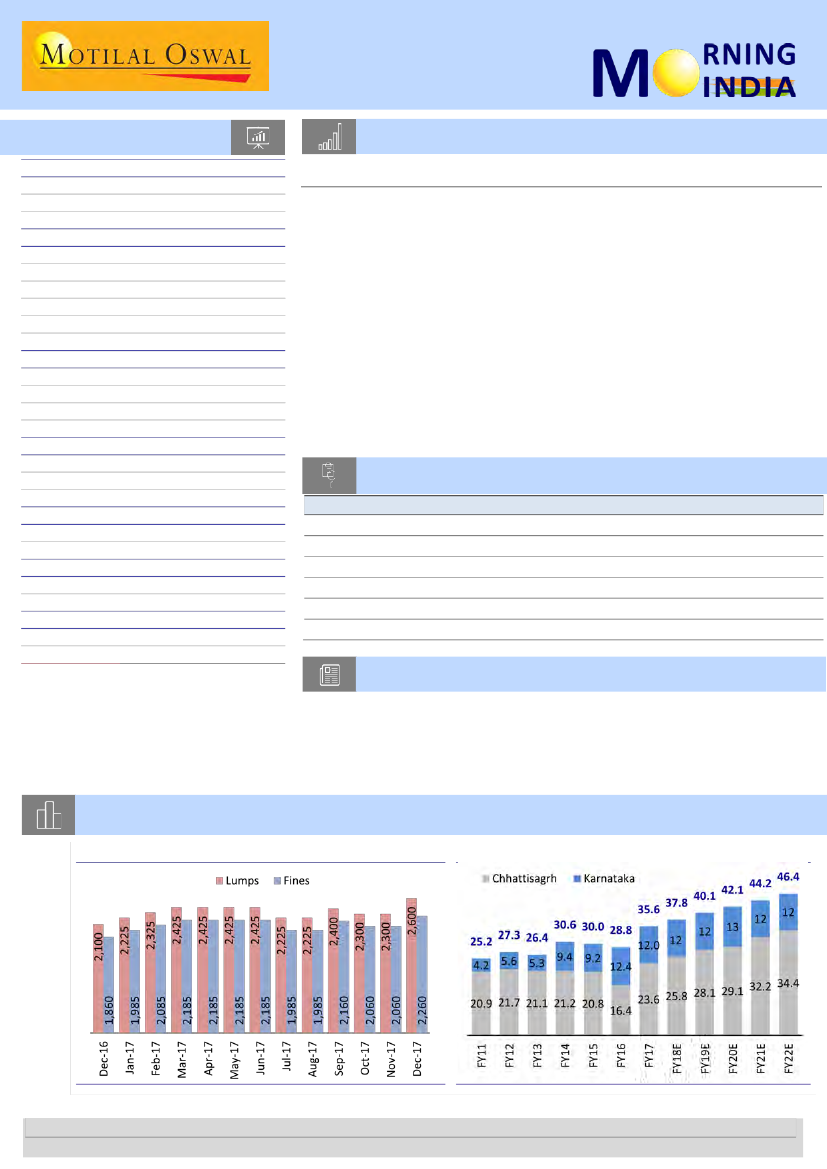

Chart of the Day: NMDC—Iron ore pricing improving

NMDC’s prices – INR/t (ex-royalty, DMF etc)

Iron ore sales – mt

Research Team (Gautam.Duggad@MotilalOswal.com)

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.