Sector Update |

Update | Financials

Sector

7 December 2017

Financials

Technology

Insolvency and Bankruptcy resolution – Speed set to accelerate

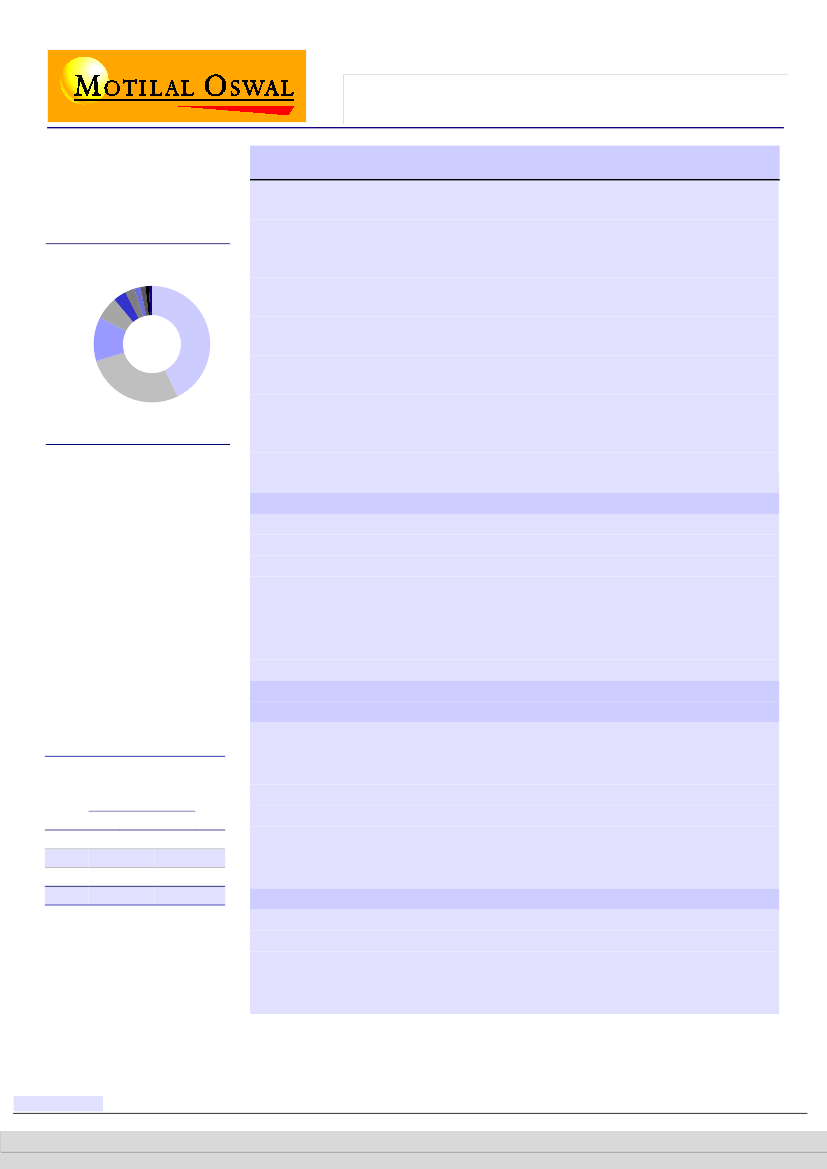

Sector-wise distribution of

combined list – by total

exposure

Although the Insolvency and Bankruptcy Code (IBC) was approved in May 2016, the

activity under this code has picked up significantly only from July 2017 after the Reserve

Bank of India (RBI) identified 12 large accounts forming 25% of the banking system’s

GNPAs for resolution under the IBC. With the resolution timeline on these cases coming

close, we met several bankers and relevant industry personnel to assess the progress and

understand the implications of this powerful law. While the recovery rate on the

announced resolution stands paltry (~90% haircut in some cases), the outlook for certain

metal and power assets is much more promising. The government and Insolvency and

Bankruptcy Board of India (IBBI) have amended the IBC and tightened the eligibility norms

in bidding for stressed assets. While these measures might lead to higher haircuts, we

believe that, over the longer term, it would prevent the re-entry of willful defaulters in the

system and promote transparency. According to our scenario analysis, resolution of NCLT

cases (RBI’s list 1 & 2) at 65% base case LGD should positively impact PSU banks’ FY19E

ABV by 6% to 26%, while private banks will see a modest ABV impact of 3% to 5%.

Auto Anc -- 6%

Textile -- 6%

Electronics --

12%

Metals --

43%

EPC -- 28%

Source: RBI, Company, MOSL

376 cases referred to NCLT; only one-third from financial creditors

A total of 376 cases have been referred to the NCLT over the first nine months of

CY17. A majority of these cases (i.e. 187) have been filed by the operational

creditors, 122 cases by the financial creditors and the remaining cases by the

corporate debtors. Resolution of these accounts is expected to be a major trigger

for corporate lenders. However, the beginning appears to be modest, with only 2

accounts taken up for resolution (at hefty haircuts), 7 accounts directed to undergo

liquidation, and another 14 witnessing further appeals.

More operational creditors

than financial creditors in the

cases referred

No. of Resolutions

Processes

Quarter

Total

Initiated by

*

**

#

FC OC

CD

Q4FY17 9

Q1FY18 31

7

59

21

35

37

125

RBI’s list 1 and 2 alone form ~45% of total GNPLs; of this, Metals, EPC and

Electronics account for ~82%

The RBI has directed banks to file 12 cases as part of its first list (of which 11 cases

were admitted), and has suggested for another 28 cases to be referred by end-

December if they are not resolved by other means. These are key accounts together

amounting to INR4t+ or ~45% of the total systemic GNPAs. We note that of this,

Metal, EPC and Electronics form nearly 43%, 28% and 12%, respectively, while

Textile and Power form 6% and 3%, respectively (refer exhibits 5 and 6 for details on

composition by major sectors).

Q2FY18 82 101

31

214

Till Date 122 167

87

376

Source: IBBI, Company, MOSL

* Financial Creditor

**

Operational Creditor

# Corporate Debtor

Many systemically important cases will get decided over next few months

While the resolution success through NCLT has been limited so far, the impending

decision on several steel assets – with many of them receiving active interest from

bidders – will make things interesting for corporate lenders. We expect resolution

process for these cases to get completed over the next few months, as the

resolution deadline draws close. Please refer exhibit 13 for admission dates.

Research Analyst: Nitin Aggarwal

(Nitin.Aggarwal@MotilalOswal.com); +91 22 3982 5540 |

Anirvan Sarkar

(Anirvan.Sarkar@MotilalOswal.com); +91 22 3982 5505

Alpesh Mehta

(Alpesh.Mehta@MotilalOswal.com); +91 22 3982 5415

| Piran Engineer

(Piran.Engineer@MotilalOswal.com); +91 22 3980 4393

7 December 2017

are advised to refer through important disclosures made at the last page of the Research Report.

1

Investors

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.