8 February 2018

Market snapshot

Equities - India

Close

Chg .%

Sensex

34,083

-0.3

Nifty-50

10,477

-0.2

Nifty-M 100

19,480

0.4

Equities-Global

Close

Chg .%

S&P 500

2,682

-0.5

Nasdaq

7,052

-0.9

FTSE 100

7,279

1.9

DAX

12,590

1.6

Hang Seng

12,433

-2.0

Nikkei 225

21,645

0.2

Commodities

Close

Chg .%

Brent (US$/Bbl)

65

-2.5

Gold ($/OZ)

1,319

-0.4

Cu (US$/MT)

6,836

-2.8

Almn (US$/MT)

2,162

-0.5

Currency

Close

Chg .%

USD/INR

64.3

0.1

USD/EUR

1.2

-1.0

USD/JPY

109.6

0.2

YIELD (%)

Close

1MChg

10 Yrs G-Sec

7.5

-0.04

10 Yrs AAA Corp

8.1

-0.04

Flows (USD b)

7-Feb

MTD

FIIs

-0.2

-0.2

DIIs

0.1

0.5

Volumes (INRb)

7-Feb

MTD*

Cash

381

451

F&O

7,270

8,988

Note: YTD is calendar year, *Avg

YTD.%

0.1

-0.5

-7.8

YTD.%

0.3

2.2

-5.3

-2.5

6.2

-4.9

YTD.%

-2.0

1.2

-5.1

-4.2

YTD.%

0.6

2.2

-2.8

YTDchg

0.2

0.2

YTD

2.0

0.4

YTD*

431

7,594

Today’s top research idea

Eicher Motors: Operating performance in line; RE margins

stable; VECV below est.

Consol. revenue grew 23.7% YoY to INR22.7b (est. of INR22.1b), with EBITDA

growth of 23% YoY to INR7.1b (est. of INR6.9b). Consol. EBITDA margin of

31.2% was in-line.

Higher depreciation and lower other income restricted PAT to INR5.2b (+25%

YoY; est. of INR5.5b).

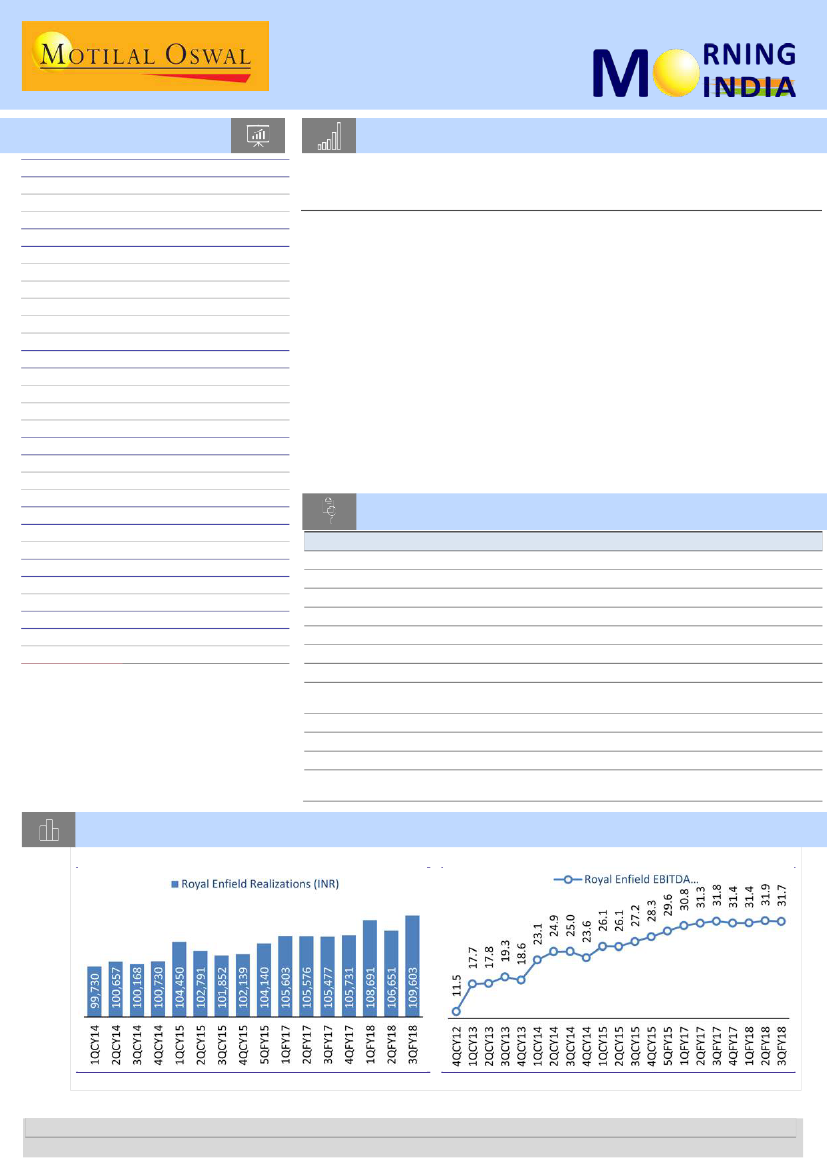

RE’s realization improved 2.8% QoQ (+3.9% YoY) to ~INR109.6k (est. of

INR106.9k).

VECV’s realization was flat QoQ (+2.4% YoY) at INR1.6m (est. of INR1.57m).

RE took price increase of 1% on 350cc models, effective Feb’18.

Plan for Phase-II at Vallam plant would be finalized in May-18; in the absence of

expansion, capacity would be 900k in FY19E.

Management expects strong growth in 7 out of top 10 states, where RE has

market share of 2-4%.

Management indicated that VECV should see continued strong demand

momentum.

Research covered

Cos/Sector

Technology

Ecoscope

Eicher Motors

Cipla

Aurobindo Pharma

Dalmia Bharat

Indraprastha Gas

Voltas

Castrol India

Thermax

Other Results

Results Expectation

Key Highlights

Early cues to CY18: Only so much acceleration from Digital?

RBI maintains status quo

Operating performance in line; RE margins stable; VECV below est.

India business shines; Margins improve strongly

Strong results; healthy growth in US and Europe business

Volumes beat; EBITDA below estimate due to higher other expenses

EBITDA below estimate; strong volume growth continues

Ahead of estimates driven by strong sales in UCP segment; project

segment margins at 7.1%

EBITDA beat led by higher volumes and realizations

Miss led by weak execution, pressure on margins

HEXW | SRF | GETD | SOIL | DITV | RIB | IPCA | BLSTR

ABB | ACC | BHEL | BHFC | CDH | CESC | GNP | GRAN | GUJS | MUTH |

PAG | PARAG | PLNG | SAIL | TCOM | TRP

Chart of the Day: Eicher Motors: Operating performance in line; RE margins stable; VECV below est.

RE’s realizations improve by ~3% QoQ

EBITDA Margin remains stable at 31.7%; -20bp QoQ

Source: Company, MOSL

Source: Company, MOSL

Research Team (Gautam.Duggad@MotilalOswal.com)

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.