14 February 2018

Market snapshot

Equities - India

Close

Chg .%

Sensex

34,300

0.9

Nifty-50

10,540

0.8

Nifty-M 100

20,150

1.4

Equities-Global

Close

Chg .%

S&P 500

2,663

0.3

Nasdaq

7,014

0.5

FTSE 100

7,168

-0.1

DAX

12,197

-0.7

Hang Seng

12,005

0.9

Nikkei 225

21,245

-0.6

Commodities

Close

Chg .%

Brent (US$/Bbl)

62

-0.1

Gold ($/OZ)

1,330

0.5

Cu (US$/MT)

6,945

2.3

Almn (US$/MT)

2,132

0.5

Currency

Close

Chg .%

USD/INR

64.3

-0.1

USD/EUR

1.2

0.3

USD/JPY

108.7

-0.1

YIELD (%)

Close

1MChg

10 Yrs G-Sec

7.5

0.01

10 Yrs AAA Corp

8.1

0.01

Flows (USD b)

12-Feb

MTD

FIIs

-0.1

-0.9

DIIs

0.2

1.3

Volumes (INRb)

12-Feb

MTD*

Cash

356

421

F&O

4,417

8,614

Note: YTD is calendar year, *Avg

YTD.%

0.7

0.1

-4.7

YTD.%

-0.4

1.6

-6.8

-5.6

2.5

-6.7

YTD.%

-6.7

2.0

-3.6

-5.5

YTD.%

0.7

2.4

-3.6

YTDchg

0.2

0.2

YTD

1.3

1.1

YTD*

425

7,634

Today’s top research idea

Sun TV - Revenue growth set to take off

Digitization gains accruing, finally

Subscription revenues are likely to grow at 16% CAGR over FY18-20, led by

digitization in Tamil Nadu. There is further upside driven by higher market

share of DTH players, growth in MSO-led subscription revenue following TRAI’s

tariff order, rising HD penetration and ARPU increase.

Higher viewership led by content rejig, shift to commission model should help

capitalize on potential ad revenue growth. Given the low base of FY17, we

expect 14% CAGR over FY18-20.

Near doubling of IPL revenue to INR2.8b bodes well. Moderate movie

investments should lead RoCE to reach ~33% by FY20.

We believe SUNTV is well poised to witness standalone revenue/PAT CAGR of

16%/24% over FY18-20. Healthy RoE of 33% and steady FCF generation should

continue to offer strong upside, valuing at 30x December 2019E EPS (~15%

discount to ZEEL), arriving at a TP of INR1,225.

Research covered

Cos/Sector

Financials

Sun TV

Hexaware Tech

Ecoscope

GAIL

Motherson Sumi

Britannia Inds

Marico

NHPC

GSK Consumer

Bank of India

Indian Bank

Other Results

Results Expectation

Key Highlights

RBI revises guidelines for stressed asset resolution

Revenue growth set to take off

Fuelling the growth engines…

Macro data in line with expectations

In-line EBITDA; LPG/HCs above est.; Trading/Petchem disappoint

Below est; Weak Op. performance, higher depreciation & tax impact PAT

Sales in-line, volumes grow in double-digits; margins surprise positively

Results broadly in line, margin pressures to continue; Maintain Neutral

Strong operating performance

Sales growth surprises on a very weak base; margins below expectations

Weak operating performance; asset quality continues to deteriorate

Strong operating performance with improving asset quality; Reiterate Buy

AMRJ | BATA | SADE | CGPOWER | AGLL | SLPA | VATW

ENDU | GDPL | GRASIM | ICNT | KNRC | NEST | PRIF | REPCO | SUNP | TPWR

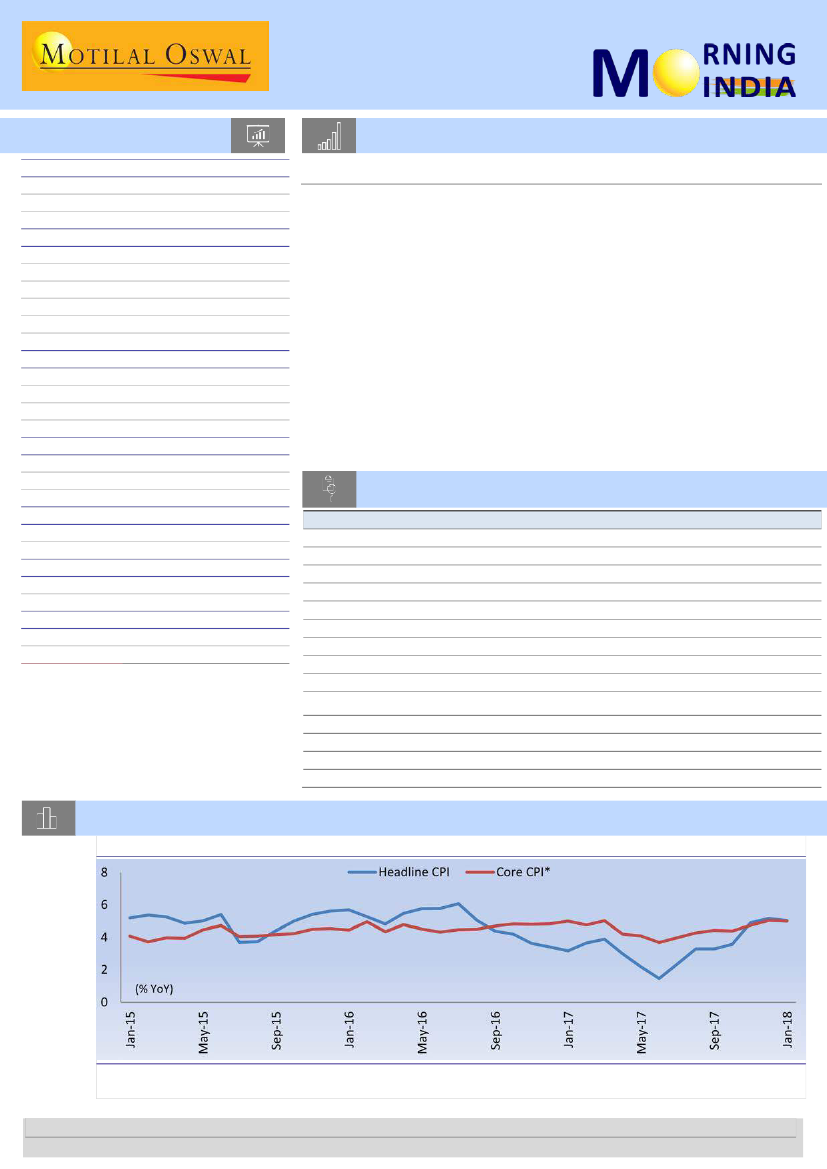

Chart of the Day: EcoScope – Macro data in line with expectations

Retail inflation eases to 5.1% in January 2018...

* Excluding F&B and F&L

Source: Central Statistics Office (CSO), MOSL

Research Team (Gautam.Duggad@MotilalOswal.com)

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.