4 April 2018

Market snapshot

Equities - India

Close

Chg .%

Sensex

33,371

0.3

Nifty-50

10,245

0.3

Nifty-M 100

19,266

0.9

Equities-Global

Close

Chg .%

S&P 500

2,614

1.3

Nasdaq

6,941

1.0

FTSE 100

7,030

-0.2

DAX

12,002

0.5

Hang Seng

12,137

1.1

Nikkei 225

21,292

-0.5

Commodities

Close

Chg .%

Brent (US$/Bbl)

68

1.2

Gold ($/OZ)

1,333

-0.6

Cu (US$/MT)

6,762

1.9

Almn (US$/MT)

1,960

-2.4

Currency

Close

Chg .%

USD/INR

65.0

-0.3

USD/EUR

1.2

-0.3

USD/JPY

106.6

0.7

YIELD (%)

Close

1MChg

10 Yrs G-Sec

7.3

-0.07

10 Yrs AAA Corp

7.9

-0.06

Flows (USD b)

3-Apr

MTD

FIIs

-0.1

2.0

DIIs

0.1

1.1

Volumes (INRb)

3-Apr

MTD*

Cash

330

312

F&O

4,333

4,062

Note: YTD is calendar year, *Avg

YTD.%

-2.0

-2.7

-8.8

YTD.%

-2.2

0.5

-8.6

-7.1

3.6

-6.5

YTD.%

1.7

2.3

-6.2

-13.1

YTD.%

1.8

2.2

-5.4

YTDchg

0.0

0.0

YTD

2.1

3.9

YTD*

386

8,114

Today’s top research idea

HDFC: Superior execution; consistent performance

Core RoE ~18% I Value of subsidiaries increasing

HDFC is not just a play on rising mortgage penetration, but also on increasing

financial literacy and financialization of savings in India. Having incubated

several subsidiaries over the past two decades, HDFC derives almost 50% of its

value from its subsidiaries, up from ~30% in FY13. In addition, there are still

some segments, like health insurance, where HDFC is to yet to enter.

The core mortgage business is on a stable growth trajectory, despite intensifying

competition. The corporate lending business, on the other hand, has witnessed a

revival over the past few quarters, after 3-4 years of modest growth.

HDFC is well equipped to take care of its own growth and growth capital

requirement of subsidiaries, with (a) large capital issuance of INR130b, (b)

expected warrant conversion of INR53.9b, and (c) capital gains from HDFCMF

(INR15b+). Of this, we expect INR85b to be utilized for HDFCB stake (already

announced) and INR45b for other ventures (new segments like health insurance,

stressed asset acquisition, investments in affordable housing projects, etc). As

there are no firm announcements for INR45b, we have valued it at 1x cash.

Despite the huge capital raising, HDFC will still maintain core RoE of ~18% over

the medium term. We use SOTP to value the company (core business at 20x

EPS and 3.2x BV) and arrive at a TP of INR2,225. Buy.

Research covered

Cos/Sector

HDFC

Bulls & Bears

M&M

BSE

Capital Goods

Key Highlights

Superior execution; consistent performance

India Valuations Handbook

: It’s a tale of caution and opportunity now

At the forefront of sustainability

Going anti-tide, pro-value; Upgrading to Buy

PGCIL ordering down 68% YoY in FY18

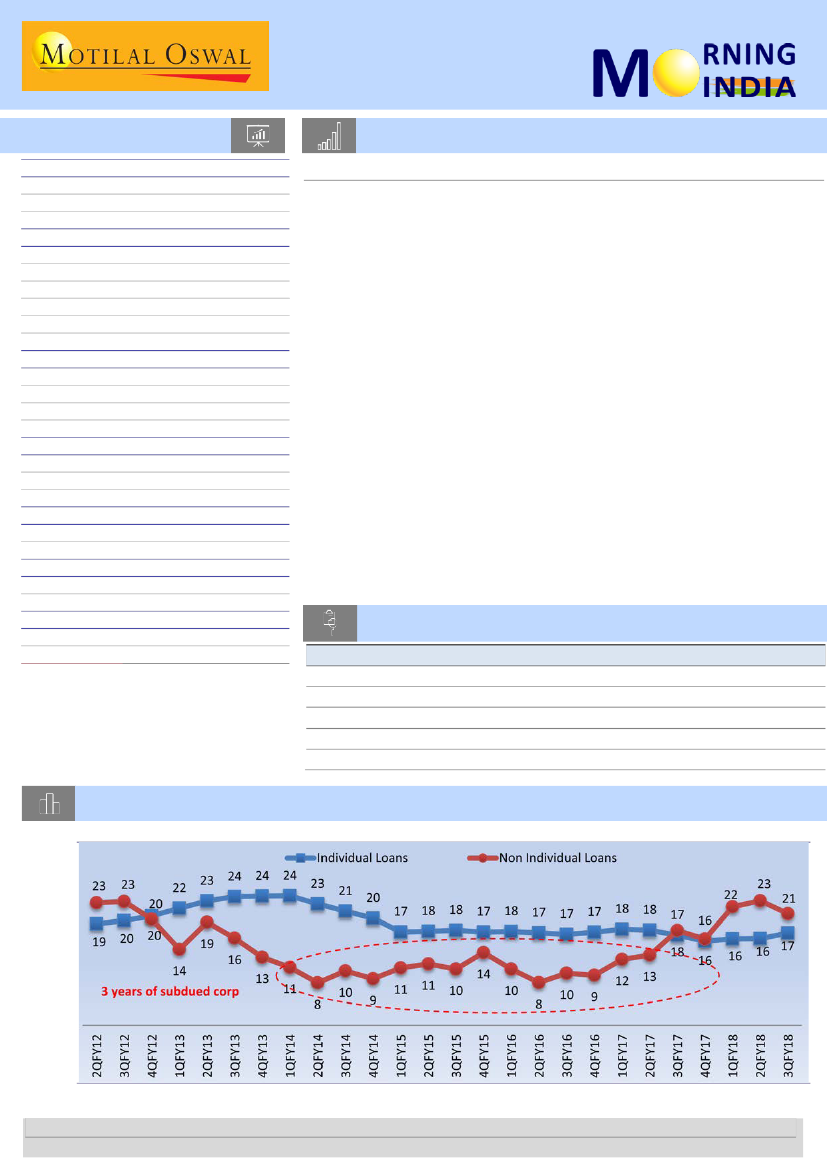

Chart of the Day:

HDFC – Superior execution; consistent performance

Growth for non-individual loans has been soft for bulk of the past three years (%)

Research Team (Gautam.Duggad@MotilalOswal.com)

Source: MOSL, Company

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.