3 May 2018

Market snapshot

Equities - India

Close

Chg .%

Sensex

35,176

0.0

Nifty-50

10,718

-0.2

Nifty-M 100

19,988

-1.5

Equities-Global

Close

Chg .%

S&P 500

2,636

-0.5

Nasdaq

7,101

0.5

FTSE 100

7,543

0.5

DAX

12,802

1.5

Hang Seng

12,194

-1.1

Nikkei 225

22,473

0.0

Commodities

Close

Chg .%

Brent (US$/Bbl)

73

-2.4

Gold ($/OZ)

1,305

-0.8

Cu (US$/MT)

6,785

0.2

Almn (US$/MT)

2,326

3.1

Currency

Close

Chg .%

USD/INR

66.7

66.7

USD/EUR

1.2

-1.1

USD/JPY

109.8

0.5

YIELD (%)

Close

1MChg

10 Yrs G-Sec

7.8

0.00

10 Yrs AAA Corp

8.4

-0.07

Flows (USD b)

2-May

MTD

FIIs

-0.1

-1.0

DIIs

0.0

1.3

Volumes (INRb)

2-May

MTD*

Cash

385

342

F&O

6,804

7,409

Note: YTD is calendar year, *Avg

YTD.%

3.3

1.8

-5.4

YTD.%

-1.4

2.9

-1.9

-0.9

4.1

-1.3

YTD.%

9.4

0.1

-5.9

3.1

YTD.%

4.4

-0.4

-2.5

YTDchg

0.4

0.5

YTD

1.2

5.1

YTD*

376

8,024

Today’s top research idea

Indusind Bank: BHAFIN’s performance on track; earnings to

accelerate post-merger

Expect RoA/RoE to recover to 2.2%/20.3% by FY20

IndusInd Bank has now entered the fourth planning cycle (FY18-20). Besides

delivering healthy profitability and gaining market share in the existing

businesses, it intends to further develop its long-cherished livelihood financing

theme in this cycle.

IIB has already taken a first step toward this by announcing a merger with its

business correspondent (BC) partner, BHAFIN. It will be able to leverage

BHAFIN’s rural network, and thus, provide last-mile financing to villages

without incurring additional cost.

We expect IIB to report healthy acceleration in earnings over FY18-20 and

project RoA/RoE of 2.2%/20.3% in FY20. Our forecasts are premised on

expectations of steady expansion in margins (FY20E: 4.7%), an improvement in

the C/I ratio (by 190bp) and controlled credit cost.

Research covered

Cos/Sector

IndusInd Bank

HCL Technologies

Hero Motocorp

Dabur India

Interglobe Aviation

Marico

Siemens

Tata Power

Gujarat Gas

Other Results

Automobiles

Results Expectation

Key Highlights

BHAFIN’s performance on track; earnings to accelerate post-merger

Guidance dampens expectations from organic momentum

In-line results; higher other expenses dent EBITDA margin

Domestic FMCG volumes up 7.7%; EBITDA margin at historical highs

Aggressive capacity addition in a lean quarter weighs on profitability

Domestic volumes and operating margins below expectations

Results below expectations due to weak execution and margins

Higher loss at Mundra and lower coal production lead to PAT miss

Ujjwala Scheme in PNG residential

DEWH | AJP | CEAT | TELX | HTML

APR-18 VOLUMES: 1. Bajaj Auto; 2. Ashok Leyland

CSTRL | HMN | HEXW | IRB | JSW | LTFH | PNBHOUSI | VEDL

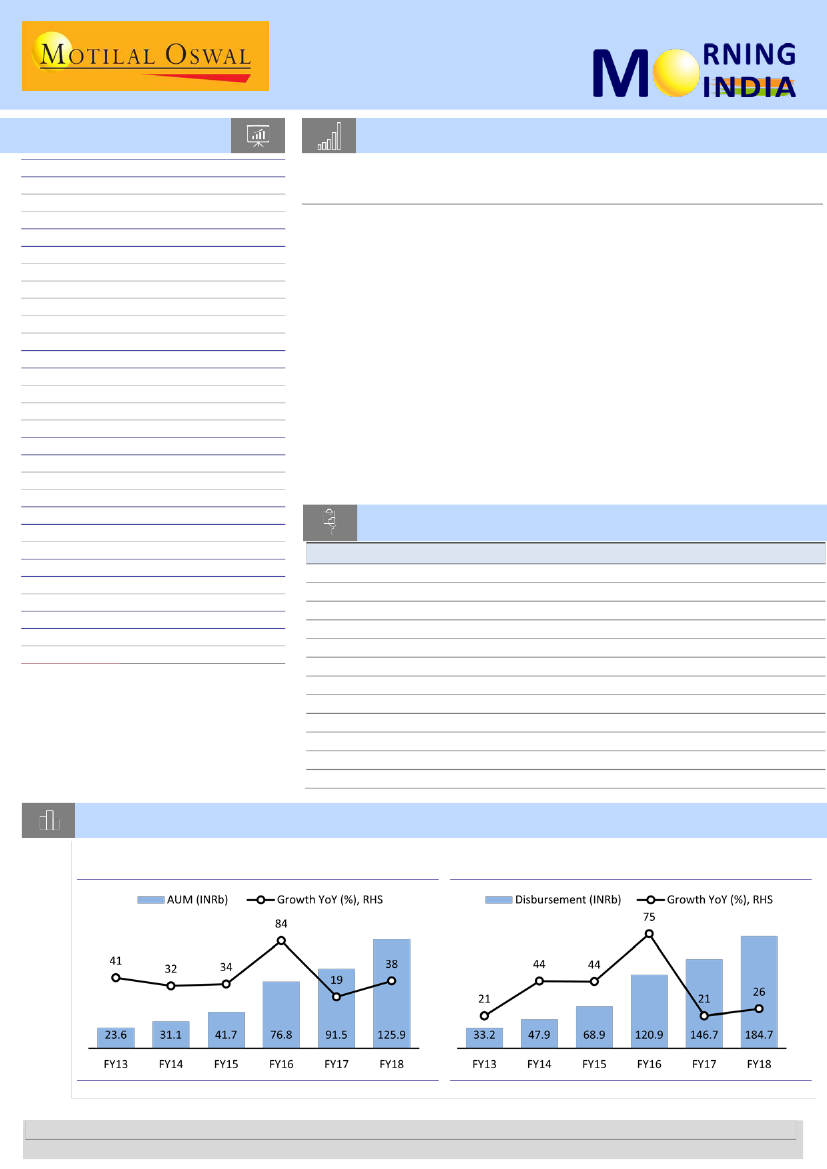

Chart of the Day: Indusind Bank – BHAFIN’s performance on track; earnings to accelerate post-merger

BHAFIN’s AUM has grown at 40% CAGR over

FY12-18…

…while disbursement has grown at 41% CAGR over

FY12-18

Source: Company, MOSL

Source: Company, MOSL

Research Team (Gautam.Duggad@MotilalOswal.com)

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.