25 May 2018

Market snapshot

Equities - India

Close

Chg .%

Sensex

34,663

0.9

Nifty-50

10,514

0.8

Nifty-M 100

18,428

-0.4

Equities-Global

Close

Chg .%

S&P 500

2,728

-0.2

Nasdaq

7,424

0.0

FTSE 100

7,717

-0.9

DAX

12,855

-0.9

Hang Seng

12,153

0.5

Nikkei 225

22,437

-1.1

Commodities

Close

Chg .%

Brent (US$/Bbl)

78

-1.1

Gold ($/OZ)

1,305

0.9

Cu (US$/MT)

6,858

0.2

Almn (US$/MT)

2,280

0.8

Currency

Close

Chg .%

USD/INR

68.3

-0.1

USD/EUR

1.2

0.2

USD/JPY

109.3

-0.7

YIELD (%)

Close

1MChg

10 Yrs G-Sec

7.9

0.02

10 Yrs AAA Corp

8.6

0.02

Flows (USD b)

24-May

MTD

FIIs

-0.1

-1.0

DIIs

0.2

2.0

Volumes (INRb)

24-May

MTD*

Cash

326

340

F&O

15,167

8,047

Note: YTD is calendar year, *Avg

YTD.%

1.8

-0.2

-12.8

YTD.%

2.0

7.5

0.4

-0.5

3.8

-1.4

YTD.%

17.2

0.1

-4.8

1.1

YTD.%

7.0

-2.4

-3.0

YTDchg

0.5

0.7

YTD

0.2

7.0

YTD*

370

8,040

Today’s top research idea

Gail India: EBITDA significantly below estimate; Petchem disappoints

Segmental analysis: Petchem disappoints due to higher input cost

Gas transmission EBIT grew 37% YoY (+6% QoQ) to INR7.1b. Gas transmission

volume stood at 106mmscmd (+5% YoY, -3% QoQ) and implied tariff at

INR1,244/mscm (-8% YoY, -6% QoQ). Base was lower due to one-time pay hike

provisioning.

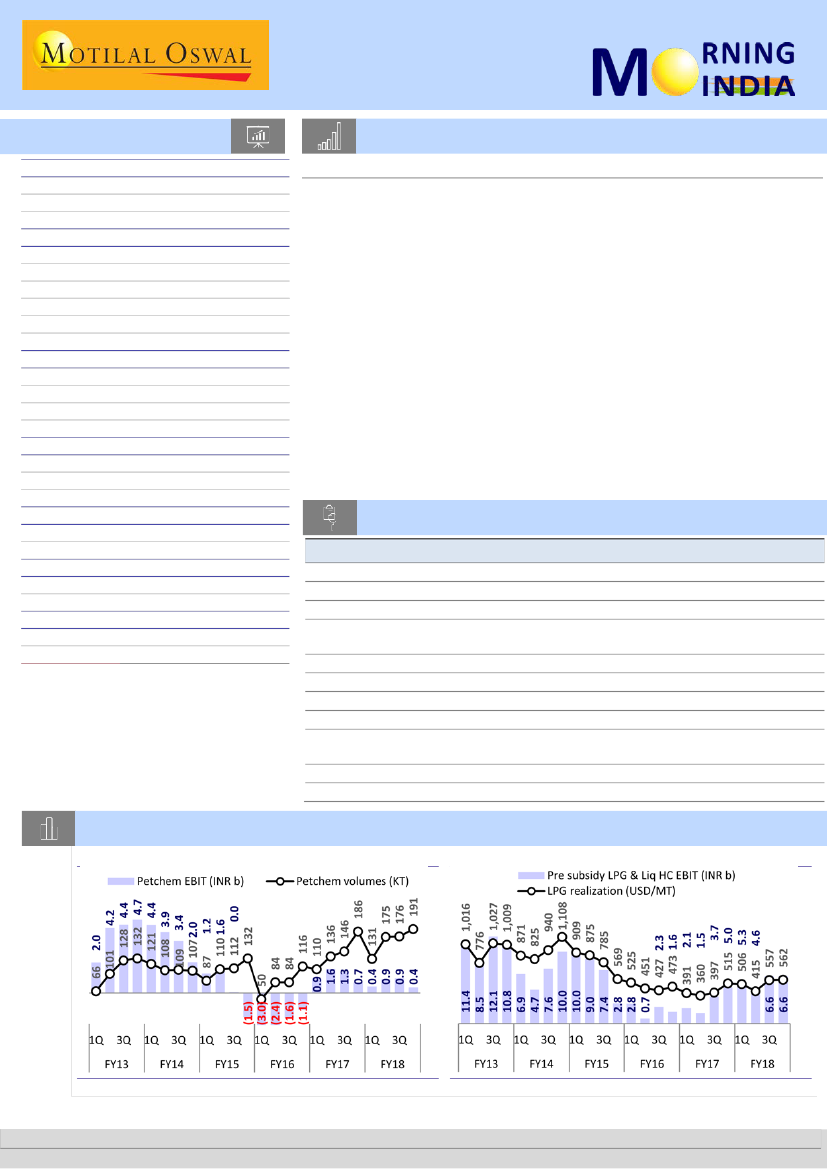

While petchem sales stood at 191kmt (+3% YoY, +9% QoQ), realization declined

to USD1,322/MT (-6% YoY, +5% QoQ). EBIT stood at INR366m (-46% YoY, -61%

QoQ), hurt by higher input cost in 4QFY18.

Due to higher availability of rich gas, LPG/liq. HC sales stood at 324tmt (+17%

YoY, -1% QoQ). Realization was USD562/mt (+9% YoY, +1% QoQ). EBIT stood at

INR6.6b (+31% YoY, flat QoQ).

Gas trading EBIT fell 41% YoY (-54% QoQ) to INR1.6b, led by trading volumes of

89.2mmscmd (+8% YoY, +2% QoQ) and trading margins of INR197/mscm (-67%

YoY, -53% QoQ). Performance was impacted by higher gas cost in 4QFY18,

which lowers GAIL’s ability to charge higher marketing margin.

Research covered

Cos/Sector

Consumer

GAIL

Pidilite Inds

Key Highlights

Rural consumption gathering pace

EBITDA significantly below estimate; Petchem disappoints

Sales ahead of expectations, EBITDA in-line

Prestige & Above volumes up 15.3% YoY; higher other income drives

United Spirits

adj. PAT beat

United Breweries Stellar numbers, 24% volume growth drives beat on all fronts

L&T Infotech

Traction intact, but upside appears capped for now

Cummins India

Lower-than-expected margins dent results

GSK Pharma

Muted revenue growth; margins stable sequentially

Engineering-led beat; Keeping rating under review until demerger is

KPIT Tech

completed

Other Results

KPIT | REPCO | NELI | KSCL | ENIL | GRAN

Results Expectation BOB | CDH | ENGR | ICEM | JAGP | PAG | PCJL | SHKL | SUNP | TECHM

Chart of the Day: Gail India – EBITDA significantly below estimate; Petchem disappoints

Petchem volumes recovered to 191kt

Realizations up YoY

Source: MOSL, Company

Source: MOSL, Company

Research Team (Gautam.Duggad@MotilalOswal.com)

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.