28 August 2018

Market snapshot

Equities - India

Sensex

Nifty-50

Nifty-M 100

Equities-Global

S&P 500

Nasdaq

FTSE 100

DAX

Hang Seng

Nikkei 225

Commodities

Brent (US$/Bbl)

Gold ($/OZ)

Cu (US$/MT)

Almn (US$/MT)

Currency

USD/INR

USD/EUR

USD/JPY

YIELD (%)

10 Yrs G-Sec

10 Yrs AAA Corp

Flows (USD b)

FIIs

DIIs

Volumes (INRb)

Cash

F&O

Close

38,694

11,692

19,774

Close

2,897

8,018

7,577

12,488

11,049

22,800

Close

75

1,211

6,092

2,073

Close

70.2

1.2

111.1

Close

7.9

8.7

27-Aug

0.04

0.16

27-Aug

330

7,831

Chg .%

1.2

1.2

1.2

Chg .%

0.8

0.9

0.0

0.8

2.5

0.9

Chg .%

0.5

0.5

0.0

0.0

Chg .%

0.4

0.6

-0.2

1MChg

0.27

0.03

MTD

0.2

0.6

MTD*

359

9,109

YTD.%

13.6

11.0

-6.4

YTD.%

8.3

16.1

-1.4

-3.3

-5.6

0.2

YTD.%

12.8

-7.0

-15.5

-8.1

YTD.%

9.8

-2.6

-1.5

YTDchg

0.6

0.8

YTD

-0.3

10.5

YTD*

357

8,418

Today’s top research Theme

SBI: Asset quality reboot done – the way forward!

We hosted Mr. Rajnish Kumar, Chairman of State Bank of India at our conference.

Key takeaways are:

IBC will take a few more months to give a sense on the recovery value. ARCs

have a poor recovery record.

Choices for NPA: a) resolution plan with the promoter; b) change of

management with the corporation and with the promoter; c) sale to ARC; and

d) NCLT.

As per management, OTS schemes with existing promoters or orderly change of

promoters leads to better recovery.

SASHAKT program is not bypassing or diluting any of the existing frameworks;

absence of strong AMC is being felt. Resolution and recovery can be better if

they are referred earlier in the IBC process by all the lenders in the ICA.

Research covered

Key Highlights

SBI | Jubilant Foodworks | Niti Aayog | Shell India | Hindalco |

United Breweries | Dalmia Bharat | Hindalco

Automobiles | Capital Goods and Electricals | Consumer | Financilas

AGIC:

– Banks; Life Insurance; NBFC | Healthcare | Media | Metals | Oil &

Management Says

Gas | Real Estate | Retail | Technology | Utilities | Midcaps/Others

Cos/Sector

AGIC: CEO Track

Takeaways

Piping hot news

FMCG consumption down, but branded item sales on the rise

FMCG consumption down, but branded item sales on the rise The country’s fast moving

consumer goods market fell 3% by volumes in the quarter ended June even as branded

products continued to grow, according to data from Kantar Worldpanel, a global consumer

research firm owned by communications and advertising giant WPP…

Note: YTD is calendar year, *Avg

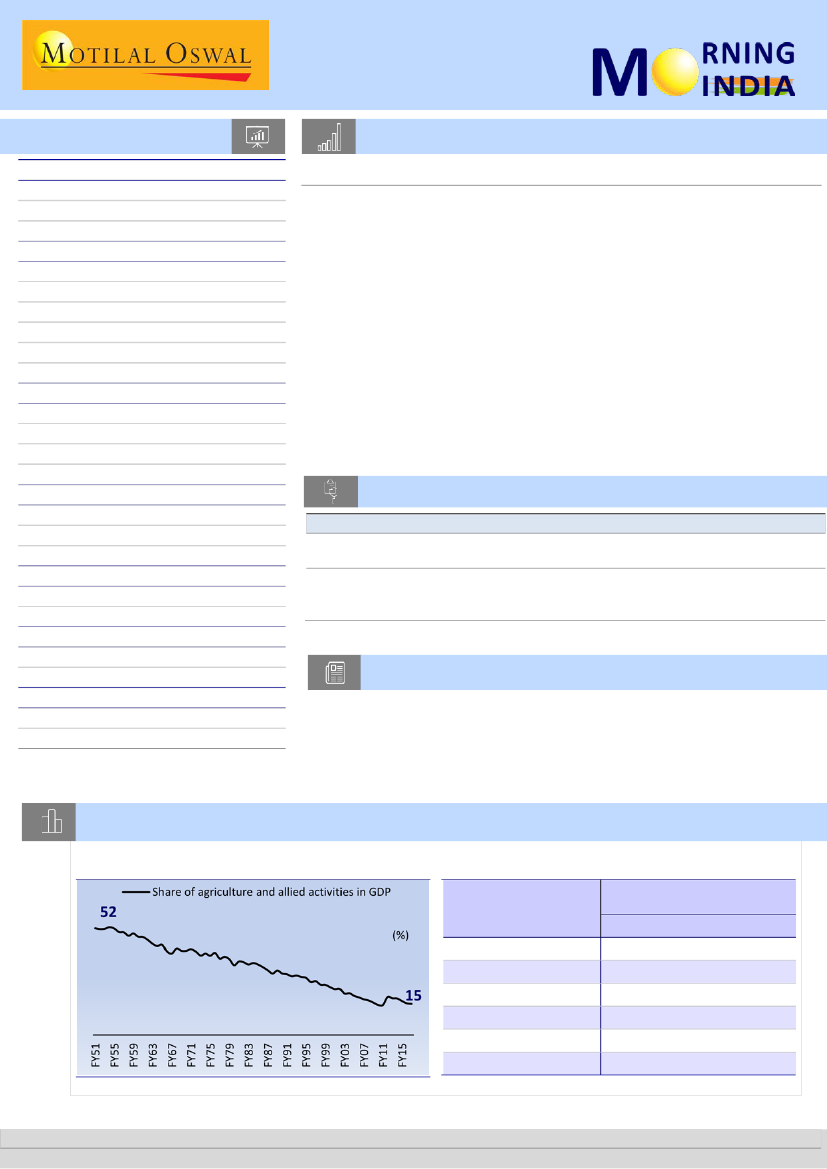

Chart of the Day: EcoKnowLedge – Will India have two budgets in 2018?

Share of agriculture in GDP has declined over the years

Share of agriculture in employment has also declined

continuously

NSS Survey period

January-December 1983

January-December 1992

January-December 1997

January-December 2003

July 2007-June 2008

July 2011-June 2012

%age employed in the primary

sector in rural areas

Male

Female

77.5

75.7

75.8

70.8

66.5

59.4

87.5

86.2

88.5

85.2

83.5

74.9

Source: State budget documents, MOSL

Research Team (Gautam.Duggad@MotilalOswal.com)

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.