Sector Update | 14 November 2018

Sector Update | Financials

India Life Insurance

Technology

I

nsurance

T

racker

Private players report steady WRP growth

Private players’ new business WRP growth was steady at ~17% YoY in Oct-18 (also flat on a

sequential basis), even as industry growth slowed down to 3.8% (+5.3% YoY in Sep-18).

Among private players, HDFC Life, Tata AIA, Birla Sunlife and Reliance Life exhibited robust

growth trends. WRP growth for HDFC Life stood at a six-month high of ~39% YoY, while it

stood at 15% YoY (v/s 17.4% in Sep-18) for SBI Life. IPRU continued showing a weak trend,

with new business WRP declining by 13% YoY (-8% over FY19YTD). On the other hand, LIC

reported a decline of 7.8% YoY in its new business WRP due to a 24% YoY fall in group

WRP. YTD growth for industry now stands at 6.4% YoY, led by growth of ~13% YoY for

private players and flat growth at LIC. We estimate private players to report WRP growth

of 16% in FY19, which implies residual growth of ~18% for the remaining months. Private

players’ market share, thus, will likely improve to 53.7% (51% in FY18).

Private players’ market share shrinks to 52.3% (51.4% in FY19YTD)

Private players’ share in total WRP contracted 428bp MoM to 52.3% in Oct-18.

Private players’ market share on an individual WRP basis stood at 56.1% (-361bp

MoM). Among private players, SBI Life and Bajaj Allianz gained maximum market

share in the individual WRP segment. However, SBI Life (13.5% market share)

remains the largest insurer based on individual WRP premiums.

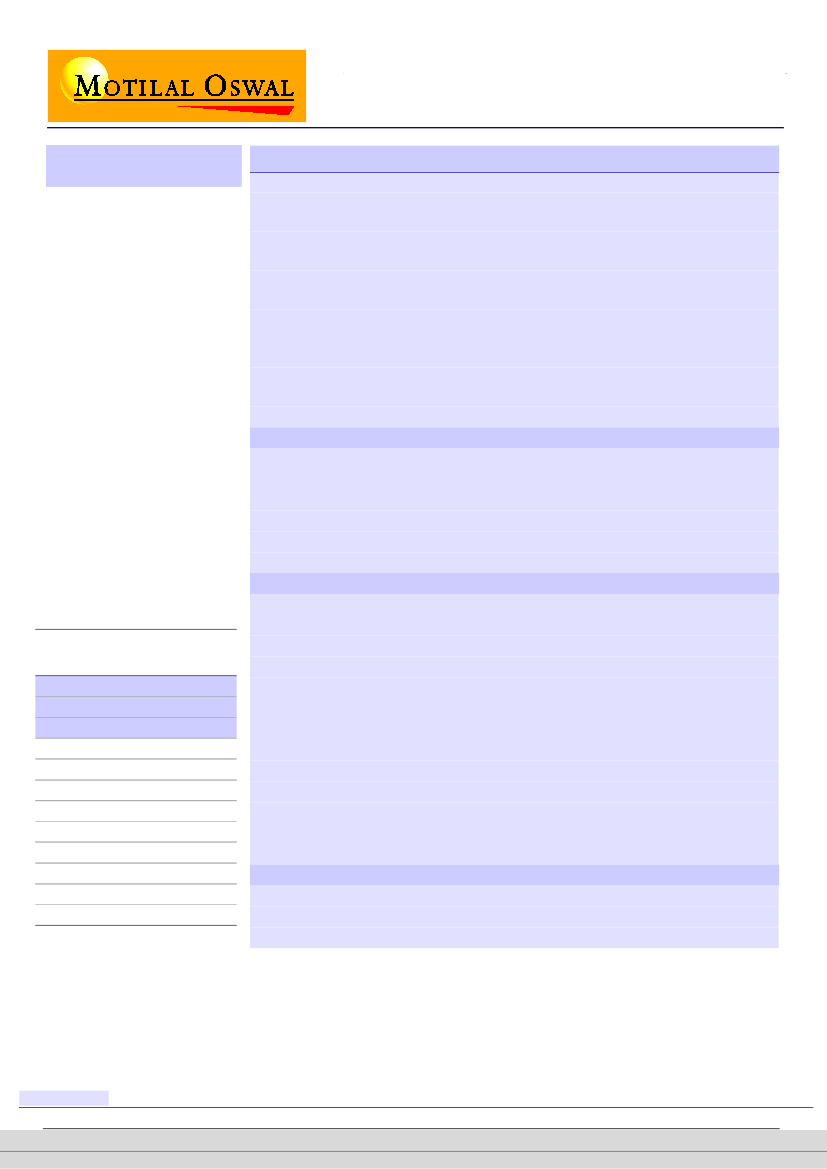

Total WRP and FY19 YTD market

share – sorted on Sep-18

Total WRP

Grand Total

Total Public

Total Private

SBI Life

HDFC Standard

ICICI Prudential

Max Life

Bajaj Allianz

Tata AIA

Kotak Life

Birla SunLife

PNB Met Life

FY19 YTD

Sep-18 mkt sh.

(%)

61,662

100.0

29,414

32,247

7,188

5,187

5,083

2,308

1,736

1,631

1,542

1,461

1,002

48.6

51.4

10.4

7.1

9.5

4.0

2.5

2.2

2.7

2.1

1.6

Top five private players account for ~66% of total private industry

The market share of top-five private players – SBI Life, ICICI Prudential Life, HDFC

Life, Max Life and Kotak Life – stands stable at ~66%. However, a few other players

like Tata AIA and more recently Birla SunLife have been showing healthy traction

and are emerging as strong contenders to become the sixth large insurer. Among

key listed players, on a WRP basis…

HDFCLIFE reported ~39% YoY growth (23% during FY19YTD) – largely in line with

our FY19 estimate.

SBILIFE reported 15% YoY growth (+11% in FY19YTD) – significantly below its

historical run-rate.

IPRU reported decline of 13% YoY (-8% in FY19YTD) – significantly below our

estimate.

Max Life reported ~28% YoY growth (+26% in FY19YTD).

Mutual fund AUM grew ~1% MoM to INR22.2t

Mutual fund AUM grew ~1% MoM to INR22.2t, led by ~15% MoM growth in money

market schemes. AUM of income funds/gold ETFs/balanced funds declined by

4.7%/2.5%/1.4% MoM, while that of ELSS funds was flat MoM at INR2.4t.

Source: Company, MOSL

Research Analyst: Nitin Aggarwal

(Nitin.Aggarwal@MotilalOswal.com); +91 22 3982 5540

| Parth Gutka

(Parth.Gutka@motilaloswal.com); +91 22 3010 2746

Alpesh Mehta

(Alpesh.Mehta@MotilalOswal.com); +91 22 3982 5415

| Yash Agarwal

(Yash.Agarwal@motilaloswal.com); +91 22 3846 6693

14 November 2018

Investors are advised to refer through important disclosures made at the last page of the Research Report.

1

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.