F

UEL

R

E

NGINES

10 June 2019

F

RIEND

O

F

T

HE

E

CONOMY

Private consumption finally moderating…

…however, income/wealth indicators have also weakened

The official GDP statistics indicate that real private consumption expenditure (PCE) grew 7.2% YoY in 4QFY19 and 8.1%

in FY19, better than the 7.4% growth in FY18 and close to the highest growth in seven years. In nominal terms too, PCE

growth of 12% was close to the highest level in six years – a trend similar to that shown by listed FMCG companies.

While these numbers don’t suggest any slowdown in PCE, monthly leading indicators paint a very different picture.

An analysis of 22 monthly indicators linked with PCE suggests that both rural and urban consumption slowed

significantly in FY19 (the former slowed more than the latter). As many as 14 out of the 22 indicators witnessed

deceleration last year.

We have been arguing that the current model of consumption-driven growth is unsustainable because it is leading to

lower savings, and thus creating financing constraints for investment recovery. The most ideal scenario for sustainable

future growth should be driven by savings-led investments, for which consumption growth has to lag income growth.

Although consumption (suggested by monthly data) appears to be moderating now, the worry is that four out of six

income/wealth-linked indicators have also shown weaker growth in FY19. If so, gross domestic savings (GDS, led by

households) may have declined further last year, keeping our concerns intact.

Motilal Oswal values your support in

the Asiamoney Brokers Poll 2019 for

India Research, Sales and Trading

team. We

request your ballot.

The strong growth in PCE

suggested by official GDP is

in line with sales growth of

listed FMCG companies but

in contrast to numerous

monthly leading indicators

of consumption.

Discord between official consumption estimates and monthly leading indicators:

Real GDP growth weakened to 20-quarter low of 5.8% YoY in 4QFY19, driven by real

investments that weakened (from double-digit growth) to 3.5%, even as private

consumption expenditure (PCE) continued growing decently at 7.2% vis-à-vis 8.1% in

3QFY19. On an annual basis, nominal PCE growth picked up from 10.6% in FY18 to

12% last year, close to its highest level in six years — a trend similar to the one seen

in aggregate sales of listed FMCG companies

(Exhibit 1-2).

Though organized/listed

companies may have benefitted from the recent reforms (also incorporated into

GDP estimates), the stronger growth in FY19 is in stark contrast to the numerous

monthly leading indicators related to consumption, which tell a different story. In

this note, we analyze 22 such indicators – divided between rural (12) and urban (10)

sector, which help us gauge possible trends in private consumption, income and

savings in the last few years.

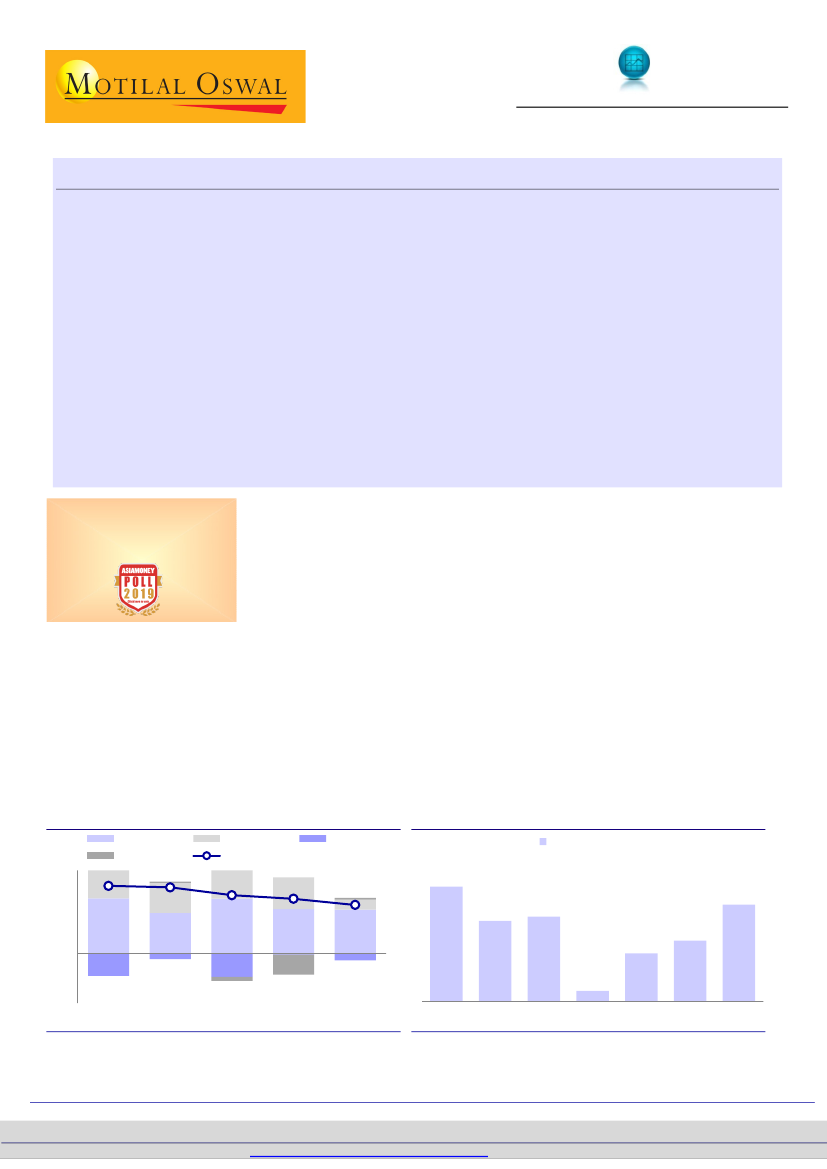

Exhibit 2:

Sales growth of 21 FMCG companies at six year

high in FY19

Sales growth (%, YoY)

15.2

1.2

5.8

5.3

(0.9)

1.4

4QFY19

FY13

FY14

FY15

FY16

FY17

FY18

FY19

10.7

11.3

6.4

8.1

12.8

Exhibit 1:

Major drivers of India’s real GDP growth (pp)

Consumption

Discrepancy

0.1

8.0

3.6

4.9

(0.7)

GCF

GDP (% YoY)

3.7

7.0

6.6

(2.8)

(0.5)

1QFY19

2QFY19

3QFY19

3.8

6.6

5.3

(0.2)

(2.4)

Net exports

10

6

2

(2)

(6)

3.9

8.1

6.6

(2.7)

(pp)

4QFY18

FY16 and FY17 data are affected by IND-AS adoption

Source: Central Statistics Office (CSO), Capitaline, MOFSL

Nikhil Gupta – Research Analyst

(Nikhil.Gupta@MotilalOswal.com); +91 22 6129 1555

Yaswi Agarwal

– Research Analyst

(Yaswi.Agarwal@motilaloswal.com); +91 22 7193 4196

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on

www.motilaloswal.com/Institutional-Equities,

Bloomberg, Thomson Reuters, Factset and S&P Capital.