19 September 2019

India Strategy

BSE Sensex: 36,093

Refer our latest India Strategy

report on - A peek into market-

cap changes since peak

Nifty-50: 10,705

The ‘In And Out’ of Institutional Flows

Institutional ownership of Indian equities has gone up by 900bp in a decade to

~35%. However, the color of institutional flows has transformed distinctly of late,

with domestic institutional investor (DII) flow significantly outpacing foreign

institutional investor (FII) flows over the last five years. Our analysis of the last 15

years also suggests a strong positive correlation of market returns with FII flows. In

this note, we discuss in detail various aspects of institutional flows and the relative

sectoral positioning.

Contrasting trends in DII and FII flows over the last decade

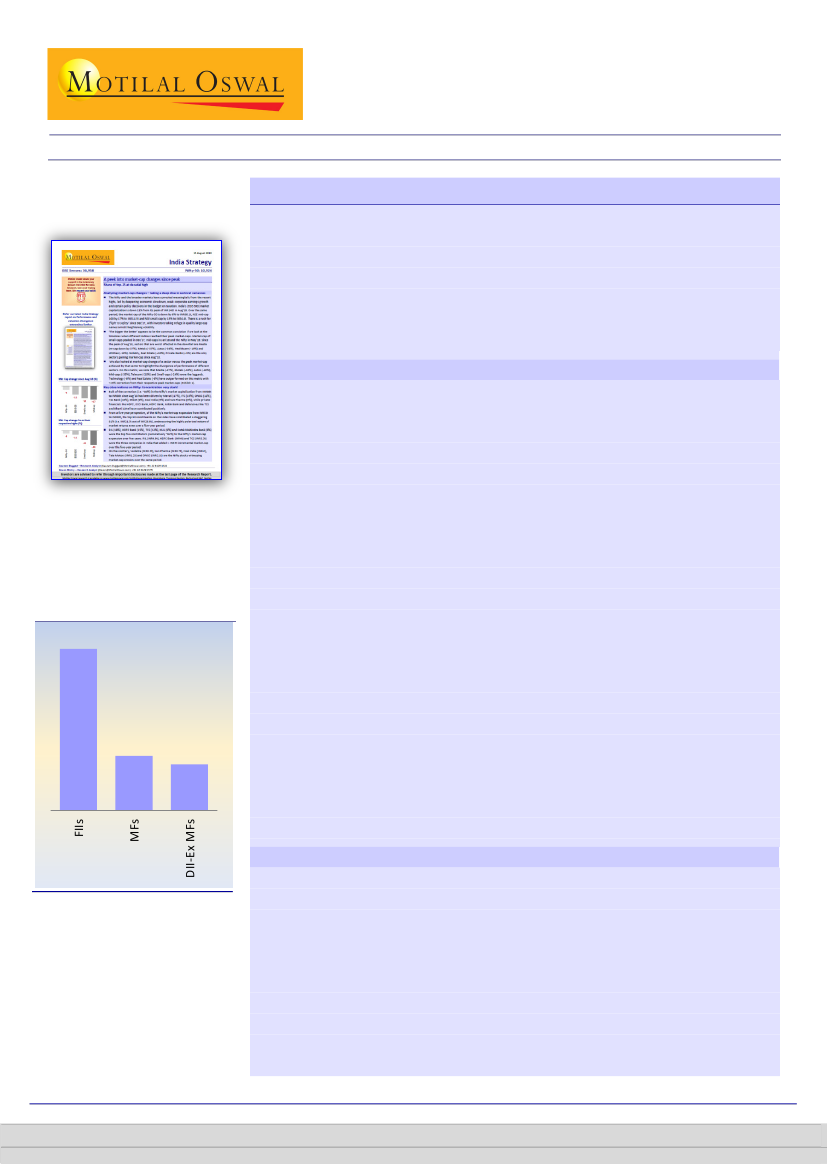

Institution value in India stands at

USD678b

418

141

119

Contrasting trends can be noticed in the dynamics of FII and DII flows in India

with a large part of the period under study being dominated by FII flows. While

FII flows tapered off post CY14, only then did DII flows pick up meaningfully,

especially mutual fund (MF) inflows. If we divide the decade (CY09-19) into two

blocks, FII flows dominated during CY09-14 with inflows of USD107b v/s DII

outflows of USD22b; DII flows dominated during CY15-19 YTD with inflows of

USD51b while FII inflows were a tepid USD16b.

FIIs:

Over the last 27 years beginning CY93, FIIs have invested USD178b in the

Indian Equity markets. The six-year period between CY09-14 was the peak with

cumulative FII inflows of USD107b. After peaking in CY14, FII inflows since then

have tapered off to a cumulative USD9.3b over CY15-18. CY19 has seen a revival

with CY19 YTD flows at USD6.5b, despite an outflow of USD4.9b since July’19.

DIIs:

Data on DII flows was made available in CY06; since then, DIIs have

invested USD55b in the Indian markets. While USD59.6b came in from Indian

mutual funds, there were outflows of USD4.6b from other domestic funds – ex

MFs. A large part of the USD55b DII flows – USD46.4b – came over the last five

years (CY14-19 YTD).

As a consequence of this, DII ownership of Indian Equities has increased from

10.5% in Mar’14 to 13.3% in Sep’19; while FII ownership has inched down

marginally from 21.8% to 21.3% over the same period. In terms of ownership of

free-float, FII ownership has decreased from 44.9% to 42.6% over a similar

period, while DII ownership has shown a meaningful jump from 21.6% to 26.6%.

Our analysis of the Nifty’s annual performance over the last 15 years v/s annual

FII flows shows that Nifty returns have a positive co-relation with FII flows.

In the 15-year period over CY04-18, FII flows have been positive in 12 calendar

years with just CY08, CY11 and CY18 witnessing outflows. Out of these 12 years,

Nifty has delivered positive annual returns in 11 out of 12 occasions, with CY15

being an exception.

On the contrary, the Nifty delivered negative returns in CY11 and CY15 despite

strong DII inflows of USD5.9b and USD10.2b, respectively. Similarly, despite DII

outflows of USD4.7b, USD10.9b, USD13b and USD4.9b in CY10, CY12, CY13 and

CY14, respectively, Nifty delivered positive returns in each of those years.

FII flows v/s market returns – strong positive co-relation

Gautam Duggad – Research Analyst

(Gautam.Duggad@MotilalOswal.com); +91 22 6129 1522

Deven Mistry – Research Analyst

(Deven@MotilalOswal.com); +91 22 6129 1575

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.