Sector Update | 9 January 2020

Cement

Price hikes in 4 quarter have

been very frequent

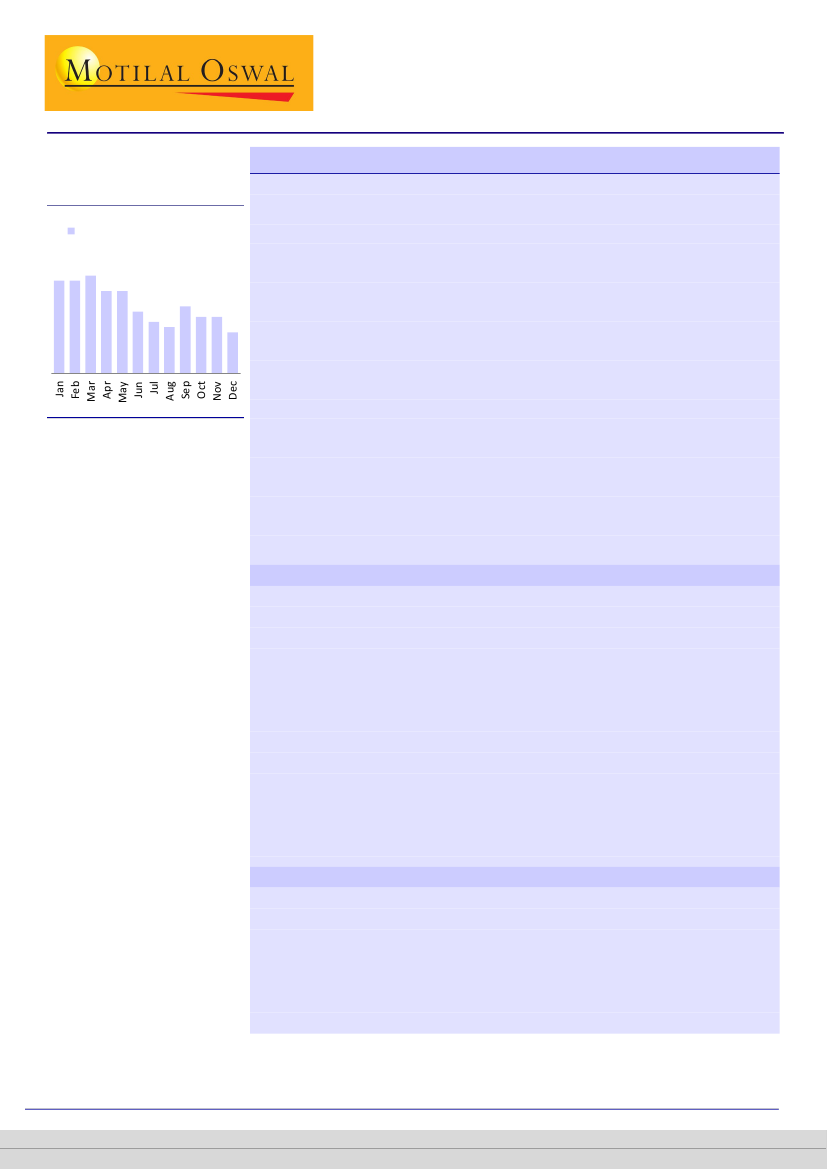

Number of instances of price

hikes in last 25 years

18 18 19

16 16

13

12

11 11

10 9

th

That time of the year again

Seasonality in prices starting to play out with hikes made this week

8

Our analysis of cement price movement over the past 25 years shows strong

seasonality with prices rising by 7% on average in first half of a calendar year but

declining by 2% in second half. We believe this is because volumes tend to be stronger

in first half, but are impacted by monsoon and festive holidays (Diwali, etc.) in other

half, leading a slowdown in construction activity.

January this year has also started on a positive note as prices have increased by

~INR10/bag (3%) in most parts of the country (according to our channel checks) after

declining by ~INR30/bag (9%) in the last six months. While some of these hikes may

get rolled back in the next few weeks, we expect the industry to continue attempting

prices hikes over the next few months as demand has been improving seasonally (i.e.

month on month) as expected.

Moreover, industry will have cost tailwind in the March quarter due to lower petcoke

price and operating leverage gains from seasonally higher volumes, which should be

further supportive of margins.

Our sensitivity analysis indicates 3-7% upgrade in EBITDA for our cement universe for

every 1% increase in price. Companies lower down the cost curve (ACC, Ambuja, India

Cement, etc.) benefit more at 5-7% from a hike given their weaker EBITDA profile.

Shree Cement accordingly benefits the least at 3%.

New year kick starts with hikes of INR10/bag across regions

The first week of Jan’20 witnessed INR10/bag of hikes across regions. All-India

cement prices are up by 9% YoY, with an increase of 13-15% YoY in north and

central India and 3-4% YoY in east and west.

While prices remained steady to INR10/bag higher in most regions of south,

Hyderabad has witnessed a hike of INR40/bag. Notably, prices in Hyderabad had

declined sharply by INR65/bag in Oct-Dec’19. Given weak demand in

AP/Telangana, we would not rule out a rollback of the hike – something which

happened in both Sept and November when hikes failed. Prices in south are

currently higher by 9% YoY including these hikes.

Our channel checks also suggest that there has been a seasonal pickup in

cement demand from Dec’19 which should be supportive of price hikes. On a

YoY basis, however, demand remains only marginally positive.

We have built in 3-5% increase in prices in 4Q for our cement universe.

Our pricing database of the last 25 years shows that price hikes tend to be

highest in the March quarter – 20 out of the past 25 years have seen sequential

price increases with an average increase of 5%.

Current prices are still lower by 6% from Apr-May’19 levels when price hikes of

INR50-60/bag were initiated in most parts of the country. Most of the decline

has been in east, west and south, while north and central India have fared

better given tighter capacity utilization there.

History suggests maximum price hikes in March quarter

Amit Murarka - Research analyst

(Amit.Murarka@motilaloswal.com) +91 22 7199 2309

Pradnya Ganar - Research analyst

(Pradnya.Ganar@motilaloswal.com); +91 22 6129 1537

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.