June 2024

India Strategy

BSE Sensex: 77,338

Refer to our strategy note on

Corporate profit to GDP –

Rebounds to a 15-year high!

Nifty-50: 23,516

Indian PSUs – Back with a vengeance!

Indian PSUs: Earnings momentum fueling the outperformance!

Rebounding in style…:

After a decade of underperformance, the Indian PSUs

have made an admirable comeback. They have marked FY24 as the year of clear

outperformance. This was evident in the sharp run-up of PSU companies and

their index outperformance compared to the Nifty-50 in the previous year.

…and galloping ahead:

Since our

previous report

on PSUs, released on 21

st

Dec’22, the PSU index has surged 113% to date. Conversely, the market

capitalization of the BSE PSU Index has galloped ~2.1x to INR69.1t from INR32.5t

between Dec’22 and Jun’24. The BSE PSU Index P/E ratio has expanded to 12.8x

from 8.7x during the same period.

As FY24 came to an end, we are revisiting our findings on Indian PSUs.

After a period of weak performance at the start of the past decade, PSUs made a

comeback and reported a strong revival in their profits in the previous five years.

The government’s infrastructure and capex push, which had gained momentum

post-pandemic, along with cleaner balance sheet, improved governance, margin

tailwinds for commodities, and burgeoning order books, have continued to drive

the PSU outperformance and their rerating, in our opinion.

During FY19-24, PSU earnings reported a 33.8% CAGR, outperforming that of the

Private Sector, which posted an 18.6% CAGR over the same period. The share of

PSUs in the profit pool expanded to 36% in FY24 after hovering in the 17-30%

range during the past few years.

Further, the earnings of PSUs during FY24

witnessed a spectacular growth of 45% YoY.

Notably, the loss pools of PSUs have reduced consistently over the last five

years.

The contribution of loss-making companies (accounting for 1% of profit

pool as of FY24 vs. 45% in FY18) has dwindled over the past few years.

The RoE of the PSU universe also jumped to 17.6% in FY24 from the lows of 5.2%

in FY18.

Sharp underperformance of the past continues to catch up:

The PSU index

posted a CAGR of 9.6%, underperforming Nifty-50 (12% CAGR) during Jun’14-

Jun’24. Notably, the majority of the gains for PSUs have occurred in the past

four years only. The BSE PSU index reported a 9% compounded decline during

Jun’14-Jun’20, but clocked an impressive CAGR of 45% during the past four

years (Jun’20-Jun’24). During FY24, the PSU index returns of +92.4% significantly

outperformed the benchmark (+28.6%). Further, the outperformance continues

as of FY25YTD; the PSU index is up by 18% vs. the benchmark (+5.5%).

A steep fall and then a laudable rise in the market cap share:

Notably, the

market cap share of PSUs in India, which dropped significantly to 10.5% in FY22

from 20.8% in FY14, has since recovered and currently stands at 17.5%. Over a

similar period, India’s market cap skyrocketed to INR389t in FY24 from INR69t in

FY14 and currently it stands at INR440t. During FY14-24, PSUs’ market cap

surged to INR66t (INR77t as of Jun’24) from INR14t, while the private sector’s

market cap catapulted to INR323t (INR363t as of Jun’24) from INR55t.

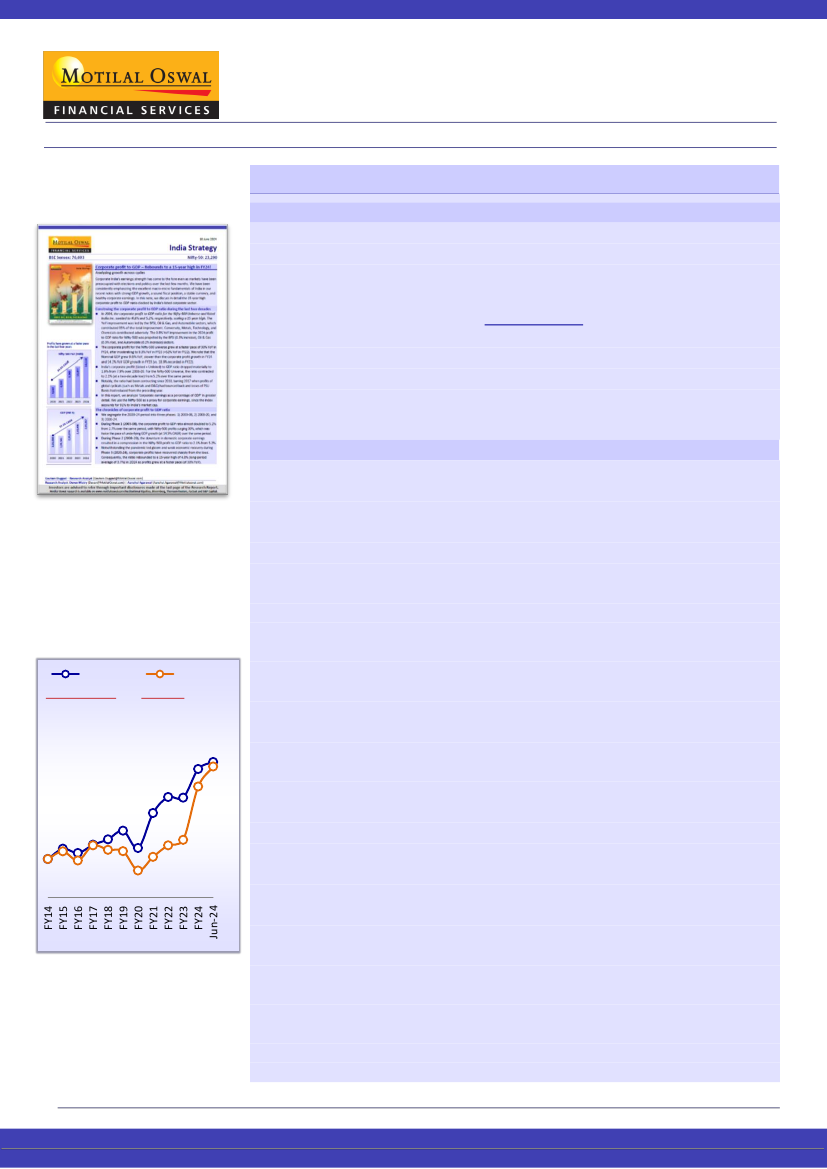

Strong business narratives and growing order book driving a rerating

PSU index has outperformed the

Nifty in FY25YTD

Nifty Index

PSU Index

CAGR:FY14-24

FY25YTD

Nifty Index: 12.8% Nifty Index: 5.5%

PSU Index: 11.1% PSU Index:18%

351

339

100

Gautam Duggad – Research Analyst

(Gautam.Duggad@MotilalOswal.com)

Deven Mistry – Research Analyst

(Deven@MotilalOswal.com)

/

Aanshul Agarawal

(Aanshul.Agarawal@Motilaloswal.com)

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.