Healthcare

Monthly

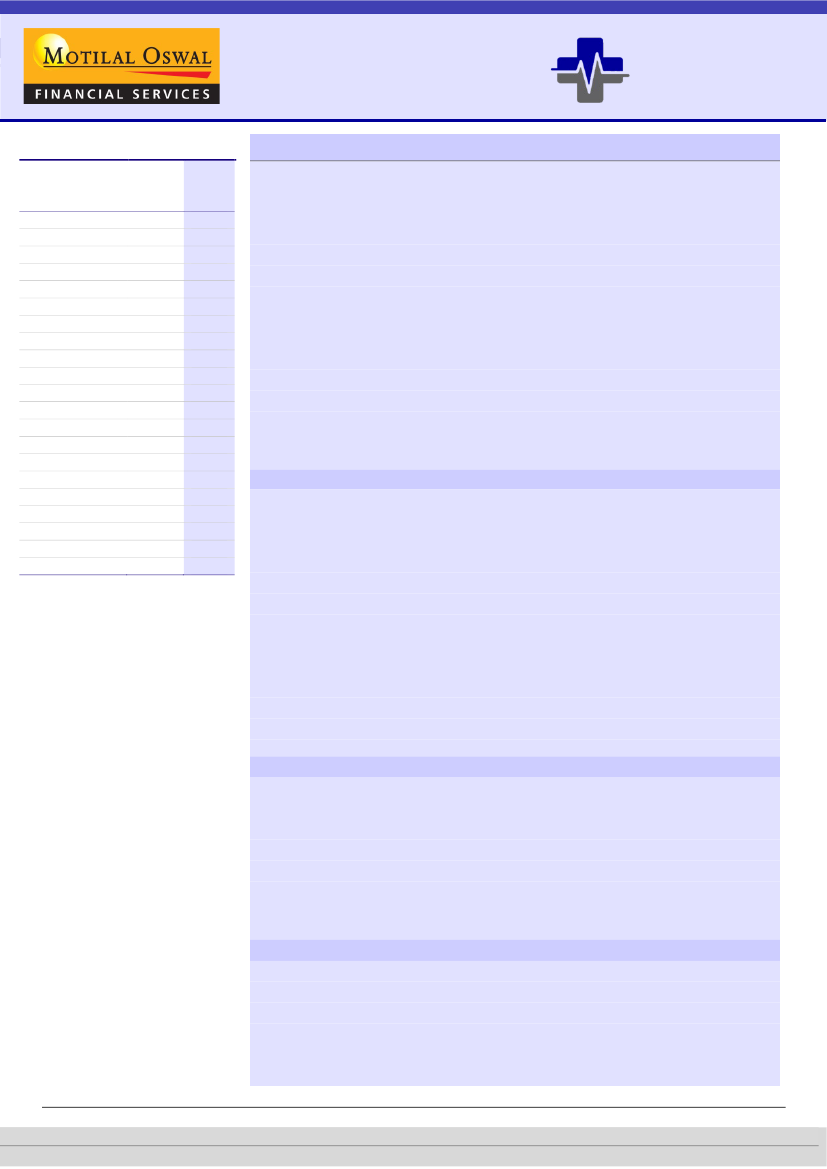

Performance of top companies in Jun’24

MAT

Jun’24

Company

growth

(%)

(%)

11 July 2024

YoY growth softens after two months of healthy growth

The India pharma market (IPM) grew 6.7% YoY in Jun’24 (vs. 9.8% in May’24 and

5.3% in Jun’23). Despite a low base of Jun’23, YoY growth was weak in Jun’24. In

fact, YoY growth trend has moderated after healthy growth in Apr-May’24.

Respiratory/Ophthal/Gynae underperformed IPM by 500bp/440bp/420bp.

Gastro-intestinal/anti-infective therapies registered healthy YoY growth of

10%/9% in Jun’24.

For the 12 months ending in Jun’24, IPM grew 7.6% YoY. This growth was led by

pricing/new launches, which contributed +4.2% YoY/2.9% YoY to the overall

growth.

Among the top 10 brands, ZERODOL-SP/PAN-D/LIV-52 registered 17%/16%/16%

YoY growth to INR520m/INR500m/INR510m in Jun’24.

Although anti-diabetic segments registered growth in Jun’24, key brands, like

Mixtrad (INR660m)/Glycomet-GP (INR660m)/Novomix (INR300m) declined

11%/5%/12% YoY in Jun’24.

In Jun’24, among the top-20 pharma companies, IPCA (up 12% YoY), Glenmark

(up 10.3% YoY), and Macleods(up 9.9% YoY) recorded notably higher growth

rates than IPM.

IPCA outperformed IPM, led by strong performance in Pain/Gastro/Antineoplast

therapies.

Glenmark outperformed IPM, led by strong performance in cardiac/Derma

therapies (16.6%/15.6% YoY).

Macleods outperformed IPM, led by double-digit growth in anti-infective/anti-

diabetic therapies.

Sanofi reported industry-leading volume growth of 5.7% YoY on the MAT basis.

Macleods Pharma registered the highest price hike of 7.4% YoY on the MAT

basis. Eris posted the highest growth in new launches (up 9.8% YoY).

On the MAT basis, the industry reported 7.6% growth YoY.

Cardiac/ Gastro /Neuro/ grew 10.5%/8.7%/8.3% YoY.

Respiratory/Gynae/Derma sales underperformed IPM by 660bp/130bp/100bp,

hurting overall growth.

For eight consecutive months, Chronic therapy has outperformed acute therapy.

The Acute segment’s share in overall IPM stood at 62% for MAT Jun’24, with YoY

growth of 6.2%. The chronic segment (38% of IPM) grew 9.8% YoY.

As of Jun’24, Indian pharma companies hold a majority share of 83% in IPM,

while the remaining is held by multi-national pharma companies (MNCs).

Both MNCs and Indian companies clocked mid-single digit growth for the

quarter.

Among MNCs, Sanofi registered the highest growth rate of 9.1% YoY, while

GLAXO posted the lowest growth rate of 2.8% in Jun’24.

IPM

Abbott*

Ajanta

Alembic

Alkem*

Cipla

Dr Reddys

Emcure*

Eris

Glaxo

Glenmark

Intas

Ipca

Jb Chemical*

Lupin

Macleods

Mankind

PGHL

Sun*

Torrent

Zydus*

7.6

8.3

8.9

3.2

6.0

7.1

8.5

7.0

9.1

0.5

10.5

11.7

12.9

9.9

6.7

9.6

8.1

0.0

8.8

8.0

6.1

6.7

6.9

9.1

5.0

5.9

3.7

6.0

5.4

7.9

2.8

10.3

8.4

12.0

7.2

6.3

9.9

8.4

9.1

8.3

4.2

8.7

IPCA/Glenmark/Macleods outperform in Jun’24

Cardiac/Gastro/Neuro lead YoY growth on MAT basis

India firms and MNCs both clock mid-single digit growth for the quarter

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

12 July 2024

1

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Tushar Manudhane - Research Analyst

(Tushar.Manudhane@MotilalOswal.com)

Akash Manish Dobhada - Research Analyst

(Akash.Dobhada@MotilalOswal.com