August 2024

India Strategy

BSE Sensex: 79,649

Nifty-50: 24,347

Nifty-50 P/E dissection: Devil is in the details!

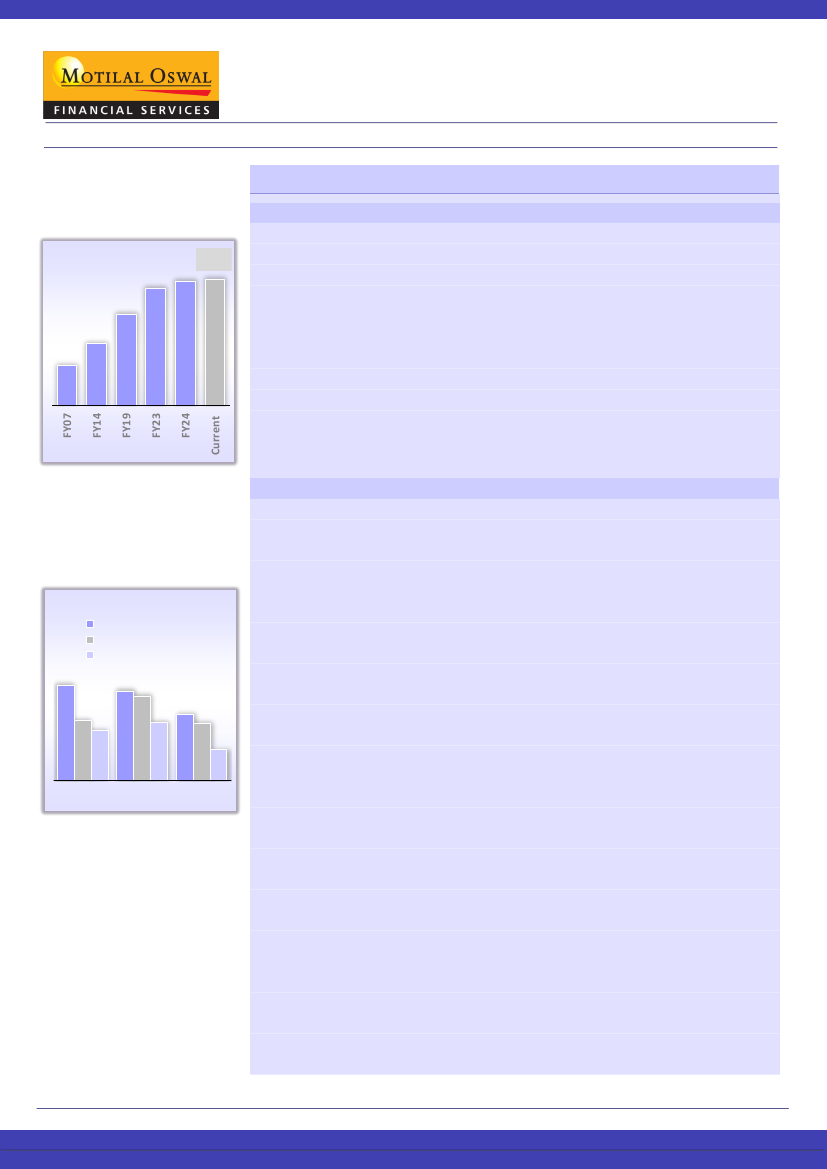

Nifty-50: 10-year rolling average

trailing P/E since FY07

Strong micro-macro dynamics – the base for premium P/E…

21.7

19.1

16.2

14.0

22.4

22.6

India commands premium valuation:

The Nifty-50 trades at 20.3x its one-year

forward earnings. Following the recent correction, it is fairly valued and within its

10-year forward average multiple of 20.4x. Compared to its EM peers, India has

been considered relatively expensive for a long period.

An anomaly in a data set

can be overlooked, but when consistent, it becomes the norm.

India enjoys its

premium valuations due to: 1) Nifty PAT, which has compounded by 25%/18%/

12% over the last 3/5/10 years; 2) a strong, continuous, and stable political setup,

with the victory of PM Narendra Modi/BJP (under NDA) for the third consecutive

term that provides policy continuity and reforms momentum, 3) a GDP growth

rate ranging between 6% and 7% during this period; and 4) healthy macros –

stable currency, twin deficits under control, peaking of interest rates, moderating

inflation print, and massive development of digital and physical infrastructure.

Re-rating and composition changes:

In FY07, the 10-year rolling average trailing

P/E was only 14.0x. It increased to 15.5x/19.1x/22.6x in FY12/FY19/Aug’24. The

re-rating has been consistent and incremental over 17+ years, in unison with the

growth potential of these stocks and earnings delivery. This trend has been

driven by the inclusion of high P/E names in retail, logistics, and consumer

sectors. Since FY07, the trailing P/E has nearly doubled for the Metals, Auto,

Technology, Oil & Gas, Cement, Telecom and Healthcare sectors. In contrast, it

has remained flat for the BFSI (ex-Insurance), Consumer, and Utility sectors.

Interestingly, as of FY14, only 14% of the stocks were trading above 30x trailing

P/E, but this figure has now surged to 50%!

Secular sectors (Pvt Banks + Consumer + Retail + Tech) have driven multiples

up between FY14 and FY19, but since then it has tapered off:

Between FY14

and FY23, the market cap contribution of secular sectors to Nifty-50 was 3

percentage points (p.p.) to 11 p.p. higher vs. its Nifty PAT contribution. However,

since FY20, the gap has been reducing. In FY24, the trends have nearly converged

as Private Banks, Consumer, and Technology stocks have underperformed. Their

earnings are likely to clock 13% CAGR over FY24-FY26E, while for the Nifty-50,

the CAGR is expected to be at 15% over the same period. Due to the higher

possibility of rate cuts by the Fed, an expected revival in consumer demand, the

emergence of AI-based themes, and a potential revival in IT spending towards

the end of CY24, the risk-reward dynamics appear in favor of it.

Nifty-50’s forward P/E in line with its LPA:

Within Nifty, the domestic and

global cyclicals trade at a one-year forward P/E of 18.2x and 15.2x, respectively.

Meanwhile, the Nifty-50 defensive basket, driven by the Consumer sector, is

trading at 29x one-year forward P/E, at a 43% premium to the index.

Of the 17 Nifty-50 sectors, three are trading at a discount

to their historical

averages, while the rest 14 trade at a premium. Private Banks/PSU Banks/NBFCs

are currently trading at 18%/13%/5% discounts to their 10-year avg. forward P/E

…however, India is always considered expensive, but why?

Nifty-50: Forward P/E multiple –

broad classification

Forward P/E - Nifty-50

Defensive

Domestic Cyclicals

Global Cyclicals

29

18

27

26

15

18

20

17

9

Aug'24

FY19

FY14

Research Analyst: Gautam Duggad

(Gautam.Duggad@MotilalOswal.com)|

Saharsh Kumar

(Saharsh.Kumar@MotilalOswal.com)

Research Analyst: Deven Mistry

(Deven@MotilalOswal.com) |

Aanshul Agarawal

(Aanshul.Agarawal@Motilaloswal.com)

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.