November 2024

India Strategy

BSE Sensex: 79,486

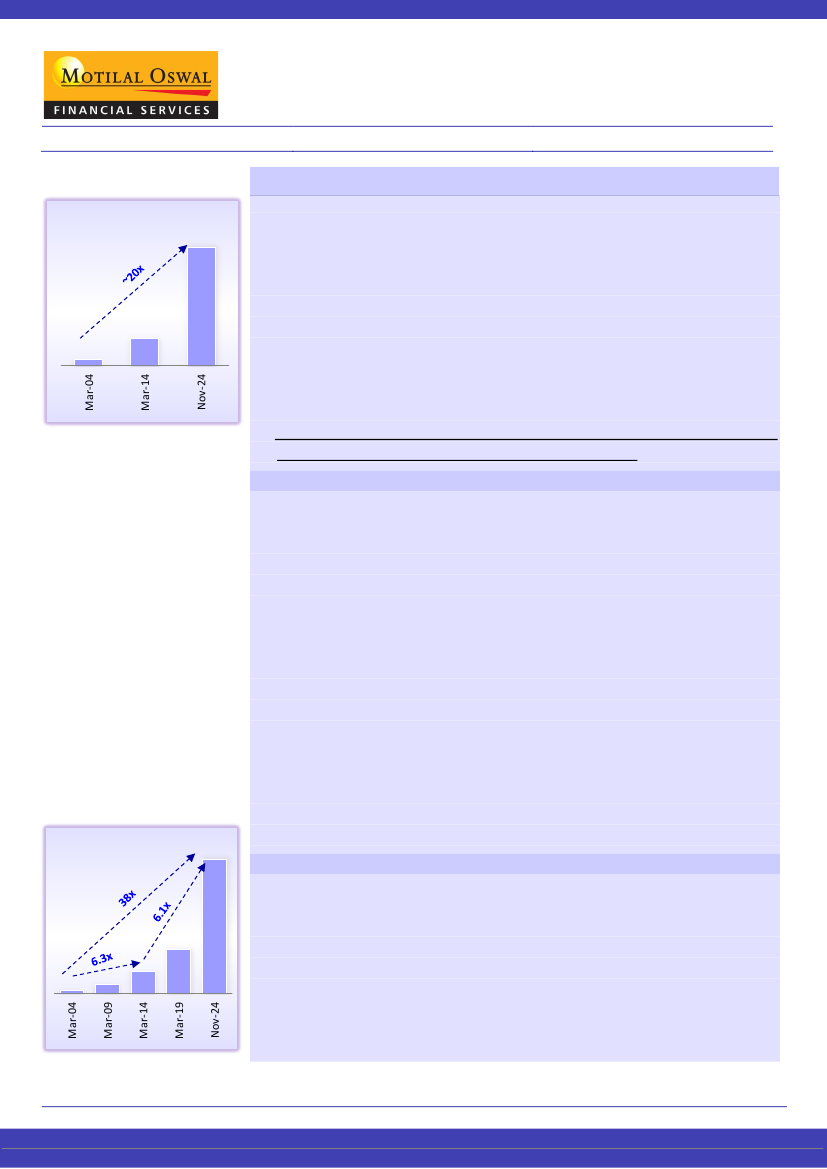

India listed market size

India market cap (USD t)

5.4

Nifty-50: 24,148

Embracing India’s Magnitude

1.2

0.3

An uncommon blend of size, growth, and diversity

Traditionally recognized for the secular growth potential, Indian equities are now

evolving, bringing fresh dimensions to the investment landscape with their

impressive size, diversity, and depth. India’s market capitalization has soared to an

impressive USD5.4t from USD1.2t in Mar’14, positioning it as the fifth-largest

market globally. Notably, smaller companies and emerging industry segments are

making substantial contributions across various sectors. Although the market is

currently experiencing a tactical breather – evidenced by a ~8% dip in the Nifty

index from its all-time high – we remain optimistic that the Indian equities will

deliver a healthy long-term compounding given the strength of corporate India’s

balance sheet and prospects of secular profitable growth.

In this report, we delve into a comprehensive analysis of the market capitalization of

Indian stocks over time, unveiling some noteworthy insights.

India’s investible universe enhances and offers wider choices to investors

India market cap growth

Listed market cap (INR t)

455

For a major portion of the 2010s, a primary concern among several large investors

was the limited investible universe of Indian equities, characterized by fewer

investible sectors, lower absolute size of companies, narrow sector breadth, and a

relatively smaller number of large-sized stocks with good depth. However, the last

five years have seen a remarkable transformation. The blazing growth in India’s

market capitalization, along with wider participation of multiple sectors and

smaller companies, as well as a wave of new issuances across sectors, has

effectively quelled many of these concerns. This evolution has paved the way for

diverse opportunities for investment across the market-cap curve and sub-sectors.

To illustrate, at present, India has

11 mega-sized companies

(~INR5t+ market

capitalization) vs. zero in 2014, with

5 companies having USD100b+

market

capitalization. The number of mid-sized companies (with market capitalization

between INR250b-INR1t) has more than quadrupled in 10 years from 50 to 209,

while the number of small-sized companies (with market cap between INR50b-

250b) stands at 466 vs. 128 in 2014. The

100

th

company (Lupin Ltd) and the 500

th

company (Symphony Ltd)

on the list today are

~8x and ~12x

bigger than the 100

th

company and the 500

th

company in 2014, respectively.

India's growing economic stature indicates a probable structural shift in global

capital allocation toward the country. As already listed Indian companies continue

to grow and new companies get listed, a sustainable cycle of discovery and value

appreciation is likely to unfold. Some of India’s mega-cap stocks (such as Reliance

Industries, HDFC Bank, and TCS) have been included in various

MSCI World

Indices.

We believe this list will expand over time, attracting interest and investments from

large, globally focused active funds. This influx should gradually enhance free float,

deepen market dynamics, and boost liquidity, paving the way for a more vibrant

Indian equity landscape.

Size does matter

12

31

75

151

Research Analyst: Gautam Duggad

(Gautam.Duggad@MotilalOswal.com) |

Abhishek Saraf

(Abhishek.saraf@MotilalOswal.com)

Research Analyst: Deven Mistry

(Deven@MotilalOswal.com) |

Aanshul Agarawal

(Aanshul.Agarawal@Motilaloswal.com)

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.