India Strategy | Review 2QFY25

India Strategy

BSE Sensex: 77,580

Refer to our Sep’24

Quarter Preview

Nifty-50: 23,533

Earnings review – 2QFY25: An insipid quarter; Commodities drag

Internals muted; Earnings downgrades>>Upgrades

Commodities dent corporate earnings:

The 2QFY25 corporate earnings scorecard

was weak, but excluding commodities, it has reported an in-line earnings growth.

Consumption has emerged as a weak spot, while select segments of BFSI are

seeing asset-quality stress. The weak government spending (flat in 1HFY25 YoY)

along with excess rainfall also impacted demand. As some of these factors self-

correct in 2HFY25, we expect the corporate earnings to recover ahead.

BFSI drives with PSU Banks leading from the front:

The aggregate earnings of

the MOFSL Universe companies were in line with our estimates and declined 1%

YoY (vs. our est. of flat YoY). Earnings for the Nifty-50 rose 4% YoY (vs. our est. of

+3%). The aggregate performance was hit by a drag from global commodities (i.e.,

Metals and O&G). Excluding the same, the MOFSL Universe and Nifty posted 12%

and 11% earnings growth vs. our expectations of +11% and +10%, respectively. The

earnings growth was driven by BFSI (+15% YoY) with PSU Banks (+34% YoY against

exp of 17% growth) and NBFC-Non-Lending (+92% YoY vs. exp of 85% growth)

leading from the front. Technology (+8% YoY), Healthcare (+17% YoY), Utilities

(+17% YoY) & Capital Goods (+17% YoY) also contributed to the growth.

Conversely, earnings growth was hindered by global cyclicals, such as O&G

(OMC’s profit plunged 92% YoY), which dipped 41% YoY, along with Cement (-

46% YoY), Chemicals (-4% YoY), and Consumer (flat YoY).

Nifty clocks single-digit growth for the second straight quarter:

Nifty delivered a

4% YoY PAT growth (vs. our est. of +3%).

Nifty reported a single-digit PAT growth

for the second successive quarter since the pandemic (Jun’20).

Five Nifty

companies – SBI, Hindalco, ONGC, ICICI Bank, and Axis Bank – contributed 140% of

the incremental YoY accretion in earnings. Conversely, BPCL, JSW Steel, Coal India,

Indusind Bank, and Reliance Industries contributed adversely to the earnings.

The beat-miss dynamics:

The beat-miss ratio for the MOFSL Universe was

unfavorable, with 38% of the companies missing our estimates, while 35%

reported a beat at the PAT level. For the MOFSL Universe, the earnings upgrade-

to-downgrade ratio has turned weaker for FY25E as 43 companies’ earnings

have been upgraded by >3%, while 121 companies’ earnings have been

downgraded by >3%. The earnings upgrade/downgrade ratio of 0.4x was the

worst since 1QFY21. Further, the EBITDA margin of the MOFSL Universe (ex-

Financials) contracted 180bp YoY to 16.2%, primarily dragged down by OMCs.

Report card:

Of the 25 sectors under our coverage, 4/12/9 sectors reported

profits above/in line/below our estimates. Of the 275 companies under coverage,

97 exceeded our profit estimates, 104 posted a miss, and 74 were in line.

A Story of Two Halves – 1HFY25 and 2HFY25E:

The MOFSL/Nifty Universes

delivered flat/ +4% YoY earnings growth in 1HFY25. Excluding Metals and O&G,

MOFSL/Nifty reported 13%/12% YoY earnings growth. For 2HFY25, we expect

MOFSL/Nifty earnings to report a growth of 9%/8% YoY. Excluding Metals and

O&G, MOFSL/Nifty is expected to report a growth of 13%/9% YoY.

FY25E earnings highlights:

The MOFSL Universe is likely to deliver sales/EBITDA/

PAT growth of 6%/5%/4% YoY in FY25. The Financials and Metals sectors are

projected to be the key growth engines, with 13% and 20% YoY earnings growth,

Motilal Oswal values your support in

the EXTEL POLL 2024 for India

Research, Sales, Corporate Access and

Trading team.

We

request your ballot.

Best Domestic

Brokerage

# Ranked Top 3

(CY21-CY23)

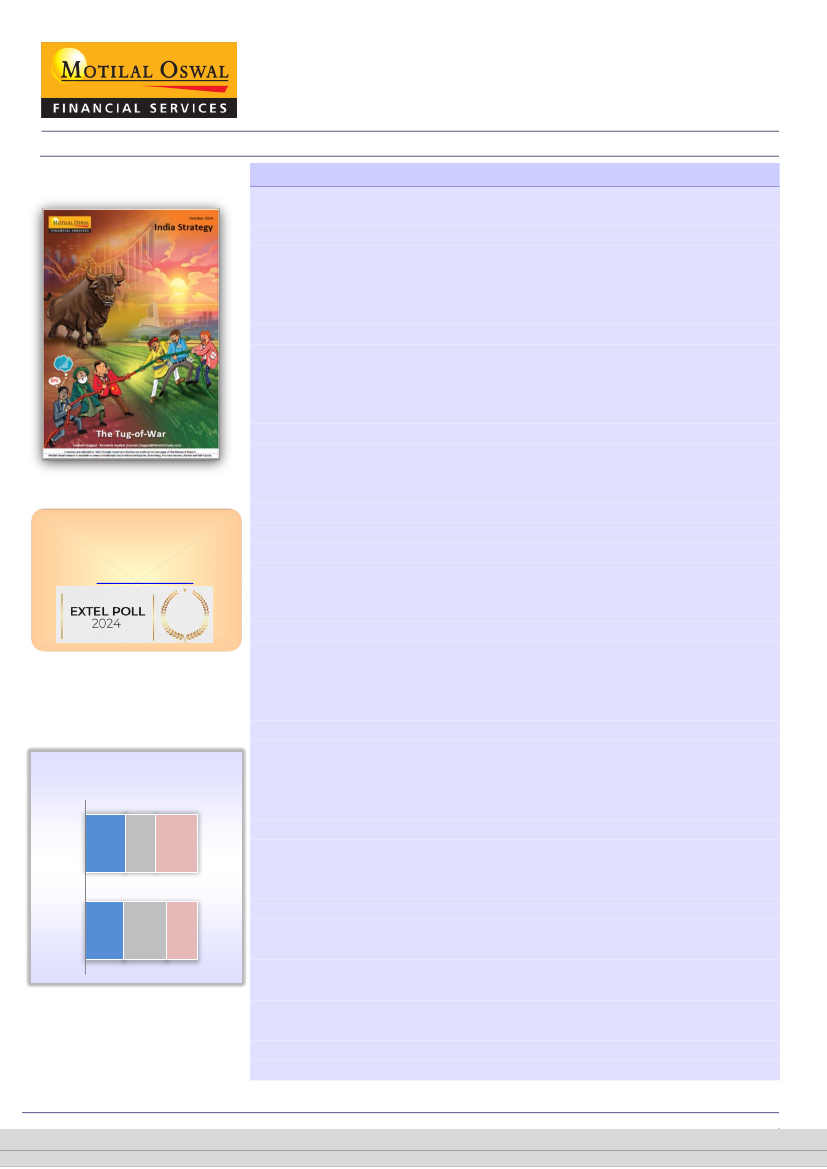

Expectations vs. delivery: 2QFY25

% of companies that have declared results

Above Expectations

In-line

Below Expectations

MOFSL

PAT

Nifty

35

27

38

34

38

28

Gautam Duggad – Research Analyst

(Gautam.Duggad@MotilalOswal.com)

Research Analyst: Deven Mistry

(Deven@MotilalOswal.com)

/

Aanshul Agarawal

(Aanshul.Agarawal@Motilaloswal.com)

November 2024

are advised to refer through important disclosures made at the last page of the Research Report.

Investors

1

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.