5 December 2024

E

CO

S

COPE

The Economy Observer

Capex Tracker: Corporate investments grow very slowly in FY24

Government and household capex healthy

After growing strongly in the past two quarters (4QFY24 and 1QFY25), our estimates suggest that corporate investments

weakened once again in 2QFY25. In contrast, government investments (center + states) picked up in 2Q after falling in

1Q, though household investments continued to grow decently. In 1HFY25, thus, while government investments declined

12.6% YoY (vs +33.8% in 1HFY24), corporate investments were up 10% YoY (vs -1.4%) and household investments rose

12.2% (vs +17.6%). This regular

update

is intended to track India’s capex trends and key drivers.

Government investments grew 4.9% YoY in 2QFY25, implying that it shrank 12.6% YoY in 1HFY25. The center’s capex

grew 15% YoY in 2QFY25, implying a fall of 13.4% YoY in 1HFY25, while states’ capex declined for the second consecutive

quarter in 2QFY25, leading to a fall of 11.5% YoY in 1HFY25. Compared to its peak of 5.1% of GDP in FY24, fiscal

investments were down to 3.9% of GDP in 1HFY25, led by a sharper fall in states’ capex (at 1.6% of GDP) and moderation

in the center’s capex (to 2.3% of GDP).

Accordingly, the government sector accounted for 12.3% of total investments in 1HFY25, similar to the pre-pandemic

years but lower than the average of 14.6% in the past four years (FY21-FY24). This also indicates that private investments

grew only 11.1% YoY in 1HFY25 vs. 7.4% in FY24 and an average of 9.7% during FY20-24.

Using data on stamp duty and registration fees collected by states, our estimates suggest that household investment

(primarily residential real estate) grew 12.2% YoY in 1HFY25, following 10.7% growth in FY24. This means that the

household sector accounted for ~44% of India’s total investments in 1HFY25, the highest since FY04.

Lastly, as a residual, we find that corporate investments (including PSEs) picked up and reported 10% YoY growth in

1HFY25, following a fall of 1.4% in 1HFY24 (and a growth of 4.3% in FY24). The share of the corporate sector, thus, inched

up ~44% in 1HFY25, compared to its two-decade low of 42.2% in FY24.

Overall, investment growth weakened in 1HFY25, primarily led by the government. On the other hand, household

investments grew decently but weaker than in the recent past. Corporate investments grew decently in 1QFY25, though

they moderated in 2QFY25. As fiscal investments pick up in 2HFY25, it would be interesting to note if the corporate and

household sectors continue to grow their investments.

Motilal Oswal values your support in

the EXTEL POLL 2024 for India

Research, Sales, Corporate Access and

Trading team. We

request your ballot.

Best Domestic

Brokerage

# Ranked Top 3

(CY21-CY23)

For the first time in two years, India’s real investments (including fixed investments,

changes in inventories, and valuables) grew slower than the total consumption

(private + government) in 2QFY25. After growing 9.4% in FY24, real investments

increased 6.5% YoY in 1HFY25, with only 5.9% growth in 2Q. Further, nominal

investments were broadly unchanged at ~34% of GDP in 1HFY25 vs 1HFY24, but

better than ~31% in the pre-pandemic years

(Exhibit 1).

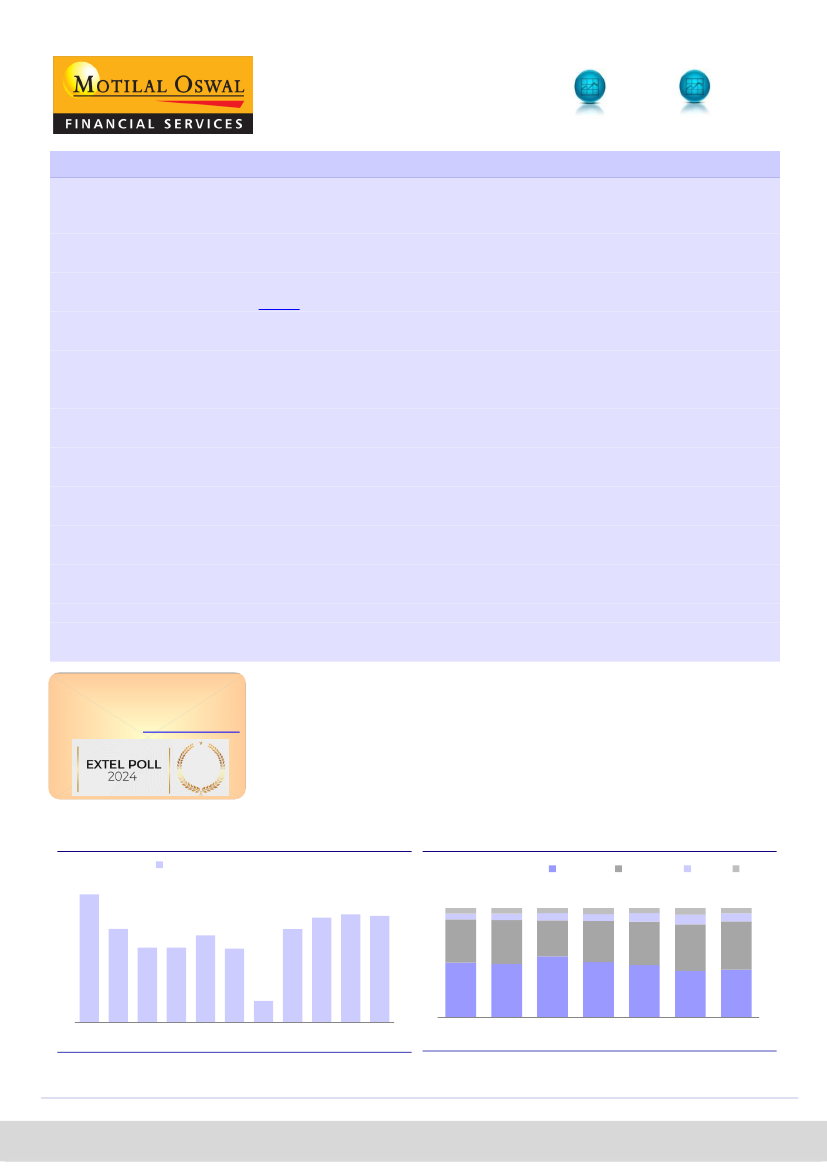

Exhibit 2: Corporate sector’s share slid in FY24, while that of

the government picked up

Sectoral investments#

(% of total)

5.2

5.4

5.2

5.9

39.7

Corporate

5.5

6.4

37.4

Household

4.8

7.7

39.5

Center

6.0

9.1

42.0

States

Exhibit 1: India’s investment rate was broadly unchanged at

~34% of GDP in 1HFY25

Total investments* (% of GDP)

35.7

32.6

30.9

30.9

32.0

30.8

32.6

33.6 33.9 33.8

4.5

6.9

32.7

5.0

7.3

43.8

39.1

26.0

50.4

49.2

55.9

50.7

48.1

42.9

43.9

1HFY15

1HFY17

1HFY19

1HFY21

1HFY23

1HFY25

1HFY19 1HFY20 1HFY21 1HFY22 1HFY23 1HFY24 1HFY25

# GFCF + Change in inventories

MOFSL estimates

Source: Various national sources, CEIC, MOFSL

* GFCF + Change in inventories + Valuables

Nikhil Gupta

– Research analyst

(Nikhil.Gupta@MotilalOswal.com)

Tanisha Ladha

– Research analyst

(Tanisha.Ladha@MotilalOswal.com)

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.