March 2025

India Strategy

BSE Sensex: 74,102

Nifty-50: 22,498

Sharp market correction offers opportunities

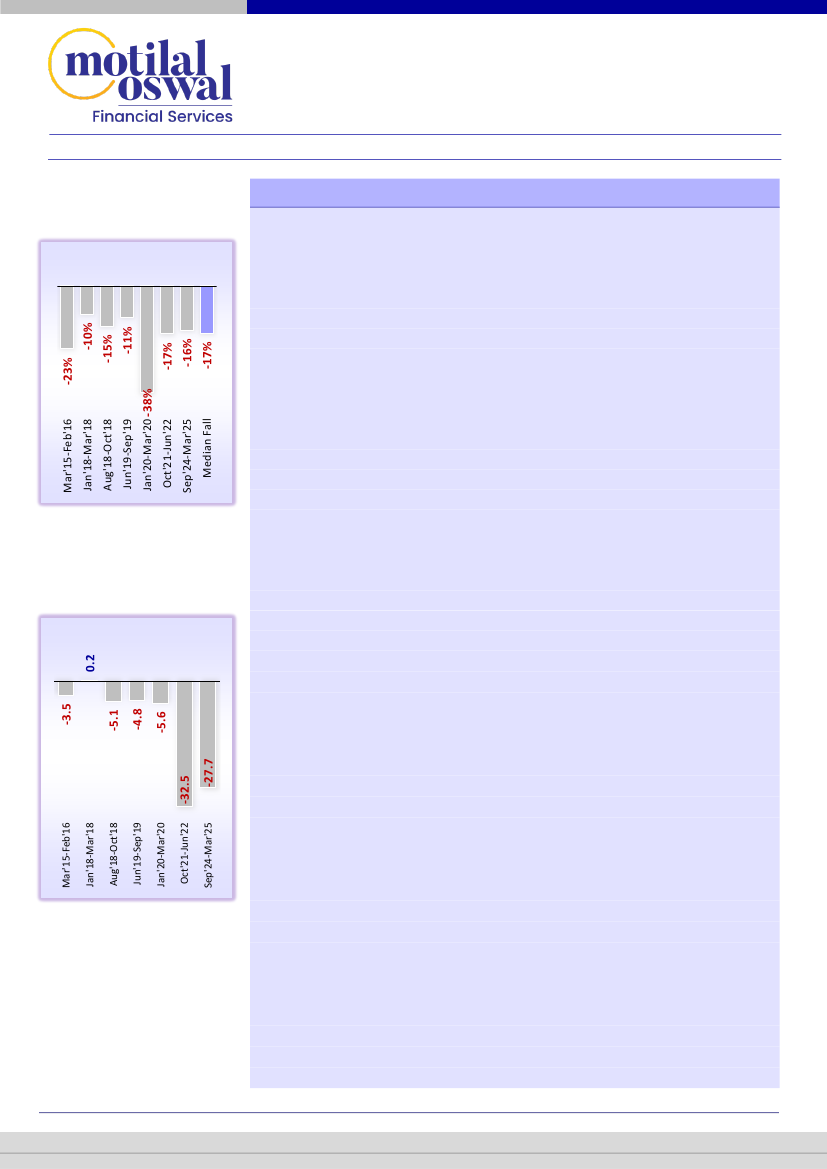

Nifty-50 correction phases

Nifty 50’s decline from

peak to trough

FII outflows during drawdowns

FII outflows during

drawdown phases (USD b)

Is the market close to a bottom?

Multiple factors suggest that the Indian

equities could be in the latter stages of correction unless any extreme

unforeseen risk materializes. We believe that the modest earnings growth so far

in FY25 should give way to double-digit growth in FY26. Market valuations have

eased, especially in large-cap stocks, with Nifty-50 trading at a ~10% discount to

LPA. India’s fiscal and monetary policies have turned stimulative, which should

support demand and sentiment. Nifty-50 has corrected ~16% since late Sep’24,

which is close to the median correction and maximum non-black-swan

correction of the past 10 years. FII selling of ~USD28b is 85%+ of the highest

selling in the past decade. Moreover, the recent global factors that are

instrumental in these corrections are also turning around, with the Dollar Index,

S&P500 and US bond yield retracing to levels closer to pre-US election results.

Buying opportunity emerging in select names:

In this report, we identify key

beaten-down names that have corrected meaningfully and currently appear out

of favor, but for which our analysts have a strong conviction over their earnings

growth, business momentum and quality of business model/management –

suggesting that the stock correction likely factors in excessive pessimism. Our

top picks identified based on the above criteria are as follows:

Large-caps: RIL,

Bharti, Hindustan Unilever, L&T, Maruti, Titan, Adani Ports, Bharat Electronics,

LTIM, Shriram Finance, JSW Energy and Polycab; SMIDs: HDFC AMC, Coforge,

Page, AU SFB, JK Cements, Ipca, Godrej Properties, Brigade, Angel One, and

Happy Forgings.

Stimulative fiscal and monetary policies should help revive demand:

The

Indian policy setting is also becoming more accommodative, which should begin

to lift demand impulse over the next few quarters. Both the monetary and fiscal

policies have pivoted to spur domestic consumption and liquidity. India’s

Finance Minister, in the FY26 Union Budget, flexed the government policy to

stimulate consumption through INR1t worth of budgeted savings for taxpayers.

Multiple monetary measures reflect RBI’s accommodative stance:

On the

monetary front, the RBI recently embarked on a rate-cut cycle after five years

(last rate cut was in Mar’20). In the lead-up to the rate cut, the RBI had also

been boosting domestic liquidity through various measures such as: 1) CRR cut

from 4.5% to 4.0% (INR1.16t), 2) OMO purchases (INR600b), 3) FX swaps

(INR450b), and 4) VRR auctions (INR42.2t). On 5th Mar’24, it announced further

measures that will potentially infuse liquidity through fresh OMOs (INR1t) and

FX swaps (~INR0.9t). Both fiscal and monetary policies have turned more

accommodative, which, in our view, will boost the demand impulse and growth

over the coming quarters.

A perfect storm:

Indian markets have corrected meaningfully over the last five

months, with the Nifty-50/Nifty MidCap/Nifty SmallCap down ~16%/21%/24%

(as of 4th Mar’25) from their peak. The broad-based correction is mainly

attributed to modest 9MFY25 earnings growth, continuous FII selling since

Oct’24 (~USD28b), a challenging geopolitical backdrop, and a strengthening

Research Analyst: Abhishek Saraf, CFA

(Abhishek.Saraf@MotilalOswal.com)

| Gautam Duggad

(Gautam.Duggad@MotilalOswal.com)

Research Analyst: Deven Mistry

(Deven@MotilalOswal.com) |

Aanshul Agarawal

(Aanshul.Agarawal@Motilaloswal.com)

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

Investors are advised to refer through important disclosures made at the last page of the Research Report.