Sector Update | 29 September 2025

Sector update | Financials

Mutual Funds

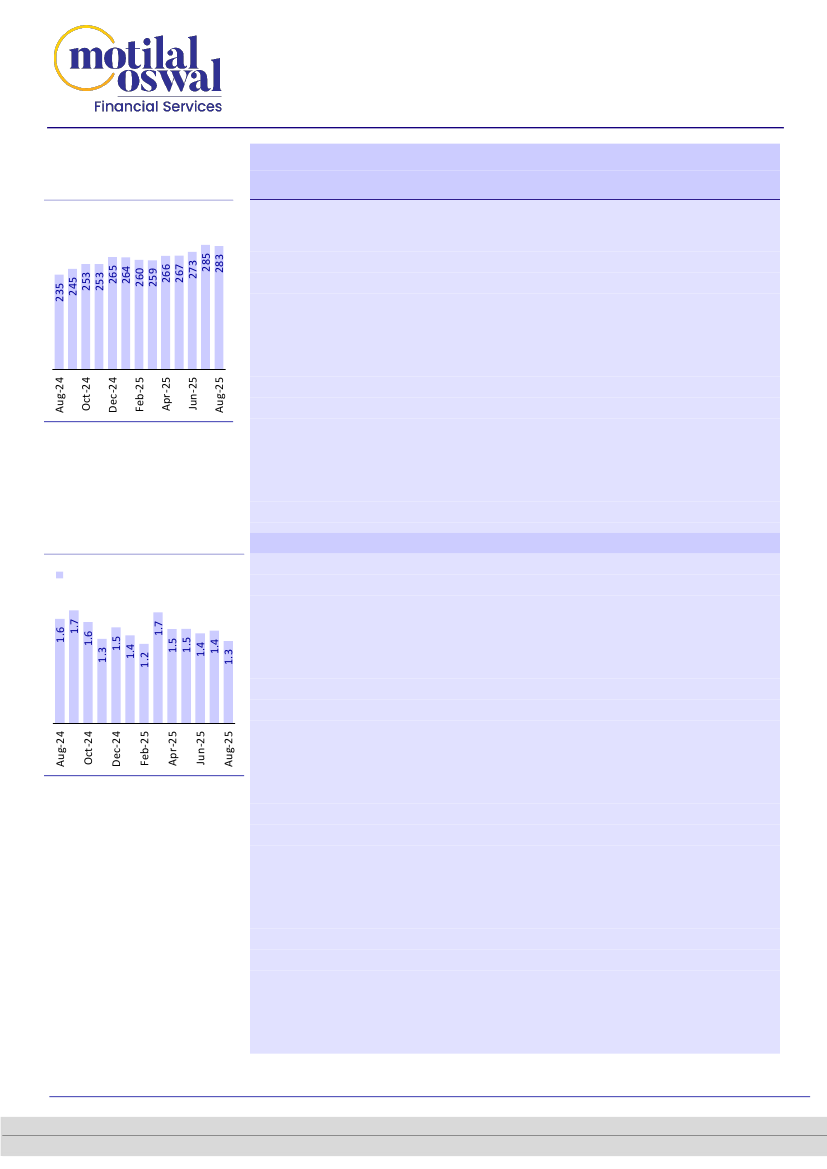

Strong trends in SIP flows

continue (INR b)

SIP traction slows down as returns dip; debt segment

still weak

We interacted with a few large mutual fund distributors (having an AUM of INR10b+),

a large B2B2C MF distributor, and institutional sales representatives to analyze

customer behavior in the prevailing market conditions.

Retail activity has seen some moderation on MF flows, considering that the 1-year SIP

returns have been negative. The trend is more pronounced with the direct channel.

Distribution-led models have experienced strong trends in the recent past. However,

competitive intensity among B2B2C channels is increasing, leading to higher sharing

with distributors.

Source: MOFSL, AMFI

Against the previous corrections in markets, wherein lump sum flows used to gather

pace, this time the activity on lump sum is on the lower side.

On the debt side, strong traction is yet to pick up in spite of the cut in interest rates

owing to the adverse taxation rules.

Structurally, we remain positive on the mutual fund-related space – AMCs,

distributors, intermediaries, and wealth managers. Our top picks in the space include

ABSL AMC, CAMS, and Nuvama.

Redemption trends steady

Equity + Hybrid redemptions as %

of AUM

Retail SIP trends weak in the recent past, more so from fintechs

Source: MOFSL, RBI

Given the weak market performance (Nifty down 4.5% over the past year), SIP

momentum among retail investors has moderated. New SIP registrations in

August 2025 were the lowest since April 2025, although encouragingly, SIP

closures have trended down, with August marking the lowest level since

November 2024.

In previous market corrections over the past five years, lump-sum flows tended

to accelerate as investors viewed declines as long-term opportunities. However,

under the current macro backdrop—characterized by tariff uncertainty and

geopolitical tensions—investors appear more cautious and are mainly staying on

the sidelines.

Operationally, disruptions on BSE StAR MF—the dominant transaction platform

for fintech players—led to multi-hour to multi-day outages in June and August

2025, blocking purchases, redemptions, and new SIP creations on apps such as

Coin. These issues likely dampened inflows for fintechs during the period.

From a business model perspective, fintechs rely heavily on digital-led customer

acquisition (advertising, incentives, and referral programs). Rising customer

acquisition costs in recent quarters, coupled with mounting profitability

pressures, have forced platforms to reduce subsidized marketing expenses,

which in turn has slowed incremental SIP additions.

Additionally, with the festive season approaching and GST rate cuts supporting

consumption demand, household spending is likely to take precedence over

financial investments. On the distribution front, after the initial round of

commission reductions by some leading AMCs, there has been little change in

commission structures in recent months.

Research Analyst – Prayesh Jain

(Prayesh.Jain@MotilalOswal.com) |

Nitin Aggarwal

(Nitin.Aggarwal@MotilalOswal.com)

Research Analyst – Kartikeya Mohata

(Kartikeya.Mohata@MotilalOswal.com) |

Muskan Chopra

(Muskan.Chopra@MotilalOswal.com)

1

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.

29 September 2025

Investors are advised to refer through important disclosures made at the last page of the Research Report.