Sector Update | 7 December 2025

Defense

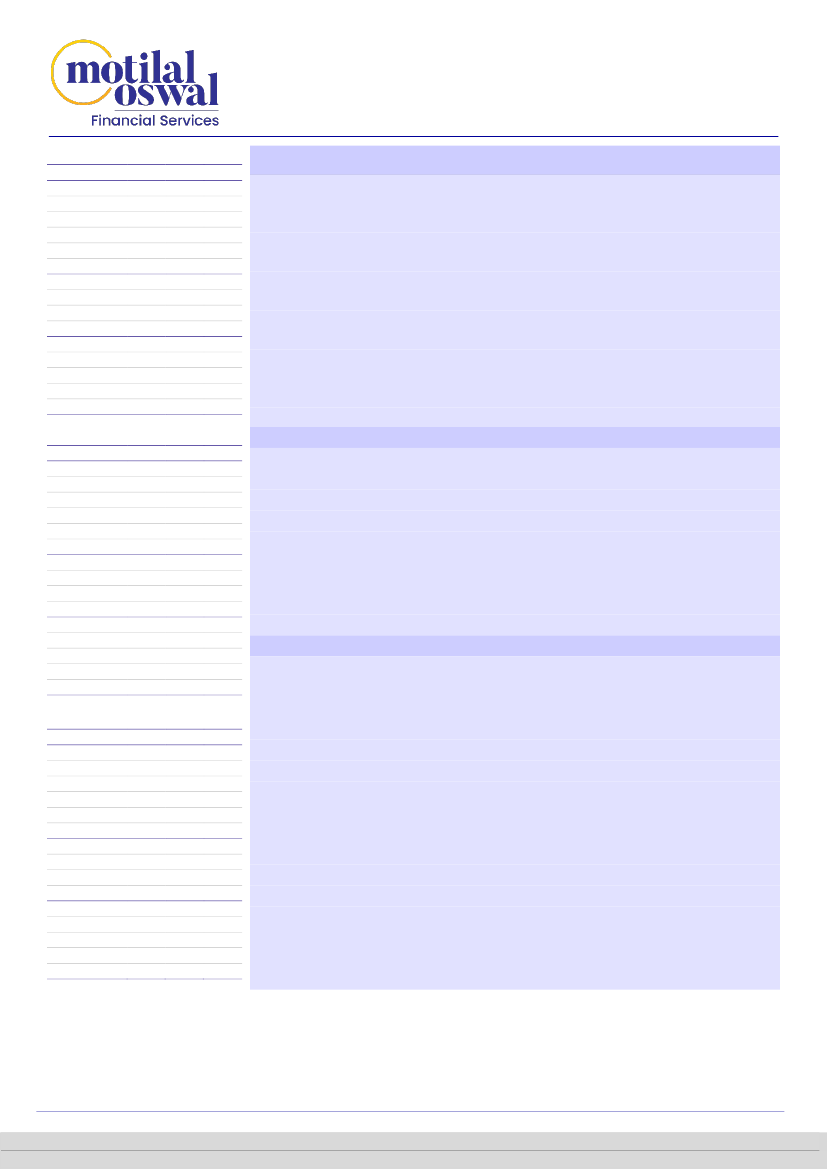

BEL - Financials & Valuations (INR b)

Y/E MARCH

FY26E FY27E FY28E

Sales

276.7 325.5 386.4

EBITDA

78.9 92.8 108.2

Adj PAT

60.8 72.1 83.8

EPS (INR)

8.3

9.9 11.5

EPS Gr. (%)

15 18.6 16.2

BV/Sh (INR)

34.3

43

53

Ratios

RoE (%)

24.2

23 21.6

RoCE (%)

27.2 25.6 23.9

Payout (%)

12.4 12.4 12.4

Valuations

P/E (x)

48.8 41.2 35.4

P/BV (x)

11.8

9.5

7.7

EV/EBITDA (x)

35.5 29.5 24.7

Div Yield (%)

0.3

0.3

0.4

HAL - Financials & Valuations (INR b)

Y/E MARCH

FY26E FY27E FY28E

Sales

375 453.4 584.6

EBITDA

111.2 129.4 159.2

Adj PAT

95.6 107.6 132.3

EPS (INR)

142.9

161 197.8

EPS Gr. (%)

14.3 12.7 22.9

BV/Sh (INR)

625.9 741.9 894.7

Ratios

RoE (%)

22.8 21.7 22.1

RoCE (%)

23.6 22.3 22.6

Payout (%)

28

28 22.8

Valuations

P/E (x)

31 27.6 22.4

P/BV (x)

7.1

6

5

EV/EBITDA (x)

22.5 18.7 14.4

Div Yield (%)

0.9

1

1

BDL - Financials & Valuations (INR b)

Y/E MARCH

FY26E FY27E FY28E

Sales

45.8 61.1 81.5

EBITDA

10.9 15.1 20.8

Adj PAT

10.4 13.9 19.1

EPS (INR)

28.3 37.9

52

EPS Gr. (%)

88.6 33.9 37.3

BV/Sh (INR)

131.6 162.5 206.5

Ratios

RoE (%)

21.5 23.3 25.2

RoCE (%)

22.1 23.8 25.6

Payout (%)

21.4 18.4 15.4

Valuations

P/E (x)

53.5 39.9 29.1

P/BV (x)

11.5

9.3

7.3

EV/EBITDA (x)

45.5 31.7 21.8

Div Yield (%)

0.4

0.5

0.5

Several catalysts at play

India’s defense sector has been witnessing many developments lately, such as ongoing

negotiations with various countries for defense deals, including export ramp-up; recent DAC

approvals; TPCR roadmap; ongoing emergency procurement; and expectations of higher

budgetary allocation. All these factors allay concerns about order inflow prospects in the

sector, and hence we expect the ordering momentum to stay strong for the sector. We expect

export opportunities to gradually open up for the sector as several defense PSUs are

developing larger platforms. Increasing indigenization supports the margin trend for

companies. We maintain our positive stance on the defense sector and we have a BUY rating

on BHE (TP: INR500, based on 45x two-year forward EPS), HAL (TP: INR5,800, premised on DCF

and 32x two-year forward EPS), and BDL (TP: INR2,000, based on 42x two-year forward EPS).

We remain Neutral on Zen Technologies.

Long-term visibility intact

We expect the defense sector to continue to benefit from 1) the expected increase

in fund allocation in the upcoming budget, supporting continued increase in TAM; 2)

AoNs worth INR7t approved during FY24-10MFY26, supporting incremental order

inflows over next few years; 3) incremental spending on defense across NATO

countries, thereby opening opportunities for defense exports; and 4) additional

momentum from the INR400b emergency procurement program under the ‘Fast

Track Procedure (FTP)’ category, which mandates significantly shorter acquisition

timelines.

Strong prospect pipeline across platforms

Our analysis of management commentaries of most defense players suggests a

strong prospect pipeline. In the

defense electronics

space, companies are

witnessing strong TAM for long-term radar, avionics, communication, and EW

orders. Bharat Electronics is expecting a subsystems order from next-generation

corvettes and an avionics order from LCA MK1A, mountain radar, Shatrughat and

Samaghat EW systems, apart from a large QRSAM order. Similarly, Astra Microwave

is expecting orders from QRSAM, Uttam radar from Tejas Mk1A, EW suite and

Virupaksha AESA radar from Su-30 MK1 upgrade, weapon locating radar, etc. In

missile and explosives,

companies expect near-term inflows from tactical missile

systems, air-defense systems, and follow-on orders for precision-strike and guided-

rocket programs. Bharat Dynamics is expecting orders from emergency

procurement, QRSAM, follow-on Astra orders from HAL, VSHORADS, etc. Solar

Industries is targeting orders from loitering munitions, counter-drone systems,

missile programs like Project Kusha as well as orders on the ammunition side from

global markets. In

defense aircraft,

HAL has recently been awarded a follow-on

order of 97 Tejas Mk1A aircraft, and the focus is on execution.

Teena Virmani - Research Analyst

(Teena.Virmani@MotilalOswal.com)

Research Analyst: Prerit Jain

(Prerit.Jain@MotilalOswal.com) |

Vatsal Magajwala

(Vatsal.Magajwala@MotilalOswal.com)

Investors are advised to refer through important disclosures made at the last page of the Research Report.

Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital.